Análise econométrica em tempo real: Modelos família ARCH para dados financeiros

Rodrigo H. Ozon

21/09/2020

Resumo

Este artigo demonstra um case de aplicação dos modelos de heterocedasticidade condicional para cotações de ativos financeiros (em especial da VALE), com integração via scrapping direto do site do Yahoo!Finance. As cotações apresentam um delay de aproximadamente 1 dia de negociação, e os scripts dos chunks do R estão todos disponíveis para replicações futuras.

Palavras-Chave: ARCH, VALE, News Impact Curve, Econometria

Introdução

Esse relatório capta dinamicamente as cotações de tres ativos

PBRPetrobrasVALEVale^BVSPIndice Bovespa

Os dados são originários do Yahoo finance. As séries temporais se iniciam em 01/01/2018 e terminam no último valor de fechamento quase que em real time.

Navegue nele para ver a aplicação de modelos econométricos de volatilidade condicional para os dados da VALE.

Iniciamos observando o caso da maior estatal brasileira, a petrolífera Petrobras:

PBR Preço de Fechamento do pregão

PBR Volume negociado

A Operação Lava Jato é um conjunto de investigações, algumas controversas, em andamento pela Polícia Federal do Brasil, que cumpriu mais de mil mandados de busca e apreensão, de prisão temporária, de prisão preventiva e de condução coercitiva, visando apurar um esquema de lavagem de dinheiro que movimentou bilhões de reais em propina.

A operação teve início em 17 de março de 2014 e conta com 71 fases operacionais autorizadas, entre outros, pelo então juiz Sérgio Moro, durante as quais prenderam-se e condenaram-se mais de cem pessoas. Investiga crimes de corrupção ativa e passiva, gestão fraudulenta, lavagem de dinheiro, organização criminosa, obstrução da justiça, operação fraudulenta de câmbio e recebimento de vantagem indevida. A Lava Jato foi apontada por críticos como uma das causas da crise político-econômica de 2014 no país. De acordo com investigações e delações premiadas, estavam envolvidos em corrupção membros administrativos da empresa estatal petrolífera Petrobras, políticos dos maiores partidos do Brasil, incluindo presidentes da República, presidentes da Câmara dos Deputados e do Senado Federal e governadores de estados, além de empresários de grandes empresas brasileiras. A Polícia Federal considera-a a maior investigação de corrupção da história do país.

^BVSP Preço de Fechamento do pregão

^BVSP Volume negociado

O índice bovespa, também chamado de IBOV, é o principal indicador médio de desempenho do mercado de ações no Brasil.

É chamado o “termômetro do mercado de ações”. Se um investidor quer saber como está sua carteira de ações, ele compara com o desempenho do índice bovespa. Se ele está melhor, pior ou com desempenho similar ao do índice.

Formado pela composição de ações das empresas com maior liquidez e maior volume financeiro negociado de todo o volume de negócios da bolsa.

VALE Preço de Fechamento do pregão

VALE Volume negociado

O rompimento de barragem em Brumadinho em 25 de janeiro de 2019 foi o maior acidente de trabalho no Brasil em perda de vidas humanas e o segundo maior desastre industrial do século. Foi um dos maiores desastres ambientais da mineração do país, depois do rompimento de barragem em Mariana.

Controlada pela Vale S.A., a barragem de rejeitos denominada barragem da Mina Córrego do Feijão, era classificada como de “baixo risco” e “alto potencial de danos” pela empresa. Acumulando os rejeitos de um mina de ferro, ficava no ribeirão Ferro-Carvão, na região de Córrego do Feijão, no município de Brumadinho, estado de Minas Gerais.

Volatilidade Variável no Tempo e Modelos ARCH

O modelo autoregressivo de heterocedasticidade condicional (ARCH) diz respeito a séries temporais com heterocedasticidade variável no tempo, onde a variância é condicional à informação existente em um determinado ponto no tempo.

O modelo ARCH

O modelo ARCH assume que a média condicional do termo de erro em um modelo de série temporal é constante (zero), ao contrário da série não estacionária, mas sua variância condicional não. Esse modelo pode ser descrito como nas Equações 1, 2 e 3.

\[\begin{equation} y_{t}=\phi +e_{t} \label{eq:archdefA14} \end{equation}\]

\[\begin{equation} e_{t} | I_{t-1} \sim N(0,h_{t}) \label{eq:archdefB14} \end{equation}\]

\[\begin{equation} h_{t}=\alpha_{0}+\alpha_{1}e_{t-1}^2, \;\;\;\alpha_{0}>0, \;\; 0\leq \alpha_{1}<1 \label{eq:archdefC14} \end{equation}\]

As Equações 4 e 5 fornecem o modelo de teste e as hipóteses para testar os efeitos ARCH em uma série de tempo, onde os resíduos e \(\hat e_{t}\) vêm da regressão da variável \(y_{t}\) em uma constante, como 1, ou em uma constante mais outros regressores; o teste mostrado na Equação 4 pode incluir vários termos de defasagem, caso em que a hipótese nula (Equação 5) seria que todos eles são conjuntamente insignificantes.

\[\begin{equation} \hat e_{t}^2 = \gamma_{0}+\gamma_{1}\hat e_{t-1}^2+...+\gamma_{q}e_{t-q}^2+\nu_{t} \label{eq:archeffectseqA14} \end{equation}\]

\[\begin{equation} H_{0}:\gamma_{1}=...=\gamma_{q}=0\;\;\;H_{A}:\gamma_{1}\neq 0\;or\;...\gamma_{q}\neq 0 \label{eq:archeffectseqB14} \end{equation}\]

A hipótese nula é que não há efeitos ARCH. A estatística de teste é

\[ (T-q)R^2 \sim \chi ^2_{(1-\alpha,q)} \]

Rodando o modelo ARCH e GARCH para os dados da VALE

ativo2[1:10,] # Gero as primeiras 10 linhas do dataset VALE.Open VALE.High VALE.Low VALE.Close VALE.Volume VALE.Adjusted

2018-01-02 12.55 12.80 12.51 12.77 19189400 9.018118

2018-01-03 12.80 12.87 12.68 12.85 20449600 9.074613

2018-01-04 13.03 13.09 12.82 12.83 22033100 9.060488

2018-01-05 12.80 13.09 12.73 13.09 20042800 9.244100

2018-01-08 13.26 13.32 13.18 13.32 17507000 9.406524

2018-01-09 13.40 13.42 13.18 13.24 31204900 9.350030

2018-01-10 13.10 13.21 13.05 13.15 16253500 9.286470

2018-01-11 13.21 13.46 13.20 13.45 15011400 9.498329

2018-01-12 13.51 13.57 13.42 13.53 19012500 9.554827

2018-01-16 13.28 13.31 13.08 13.17 40821800 9.300596Cl(ativo2) # Gero os dados para aqueles que desejem baixar por aqui VALE.Close

2018-01-02 12.77

2018-01-03 12.85

2018-01-04 12.83

2018-01-05 13.09

2018-01-08 13.32

2018-01-09 13.24

2018-01-10 13.15

2018-01-11 13.45

2018-01-12 13.53

2018-01-16 13.17

...

2023-05-26 13.26

2023-05-30 12.76

2023-05-31 12.68

2023-06-01 13.04

2023-06-02 13.68

2023-06-05 13.61

2023-06-06 13.74

2023-06-07 13.94

2023-06-08 14.09

2023-06-09 14.04Vo(ativo2) # Gero os dados para aqueles que desejem baixar por aqui VALE.Volume

2018-01-02 19189400

2018-01-03 20449600

2018-01-04 22033100

2018-01-05 20042800

2018-01-08 17507000

2018-01-09 31204900

2018-01-10 16253500

2018-01-11 15011400

2018-01-12 19012500

2018-01-16 40821800

...

2023-05-26 19326400

2023-05-30 30416300

2023-05-31 45251700

2023-06-01 52730200

2023-06-02 29286200

2023-06-05 18834400

2023-06-06 23116100

2023-06-07 24257200

2023-06-08 15324000

2023-06-09 26761600# Voce pode usar o seguinte comando para exportar esse dataset

write.csv(ativo2, file="VALE.csv")

library(xlsx)

write.xlsx(ativo2, file="VALE.xlsx")

#https://www.guru99.com/r-exporting-data.html#1 Após vermos os precos de fechamento e volume, obtenho o log retorno dos precos

dlnVALEclose <- diff(log(Cl(ativo2)), lag=1) #ln(Pt/Pt-1)

dlnVALEclose<-dlnVALEclose[-1,]

presAnnotation <- function(dygraph, x, text) {

dygraph %>%

dyAnnotation(x, text, attachAtBottom = TRUE, width = 300, height=20)

}

dygraph(dlnVALEclose, main = "Retornos logarítmicos dos preços de fechamento VALE")%>%

dyAnnotation("2019-01-25", text = "A", tooltip = "Rompimento da barragem em Brumadinho")%>%

presAnnotation("2019-01-25", text = "Rompimento da barragem em Brumadinho")%>%

dyShading(from = "2019-01-25", to = "2019-02-26")%>%

dyAnnotation("2020-03-02", text = "A", tooltip = "Corona Day")%>%

presAnnotation("2020-03-02", text = "Corona Day")%>%

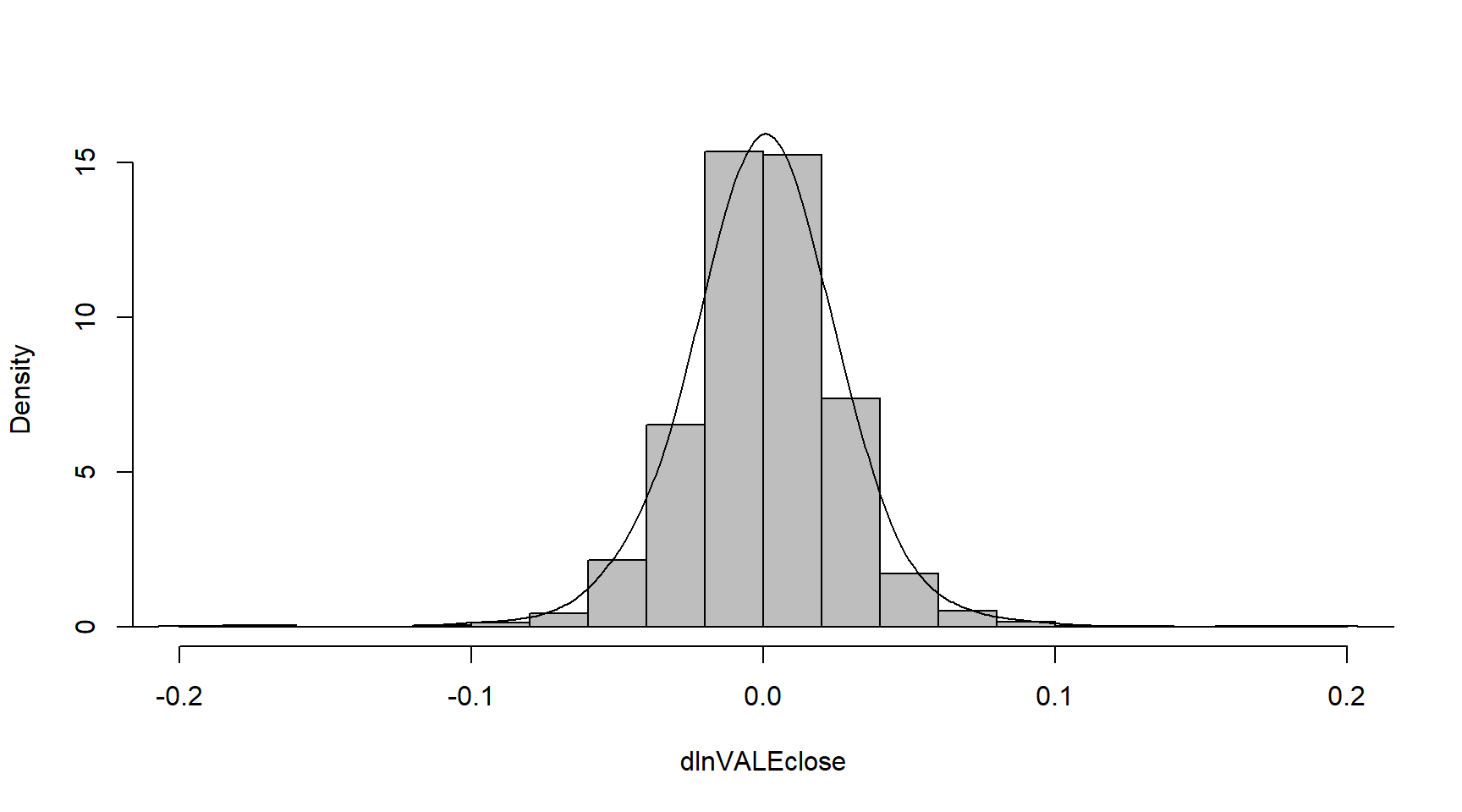

dyShading(from = "2020-03-02", to = "2020-04-27") #Grafico dos retornosAgora observo o padrão da distribuição dos log retornos:

hist(dlnVALEclose, main="", breaks=20, freq=FALSE, col="grey")

lines(density(dlnVALEclose, adjust=2, col="blue"))

Vamos iniciar carregando os pacotes necessários do R:

#rm(list=ls()) #Removes all items in Environment!

library(FinTS) #for function `ArchTest()`

library(rugarch) #for GARCH models

library(tseries) # for `adf.test()`

library(dynlm) #for function `dynlm()`

library(vars) # for function `VAR()`

library(nlWaldTest) # for the `nlWaldtest()` function

library(lmtest) #for `coeftest()` and `bptest()`.

library(broom) #for `glance(`) and `tidy()`

#library(PoEdata) #for PoE4 datasets

library(car) #for `hccm()` robust standard errors

library(sandwich)

library(knitr) #for `kable()`

library(forecast) Vamos primeiro realizar, passo a passo, o teste ARCH na variável VALE.Close. Iremos transformar os dados numa série temporal para leitura do R:

library(dynlm)

rTS <- ts(dlnVALEclose) # A funcao ts eh o mesmo que timeseries

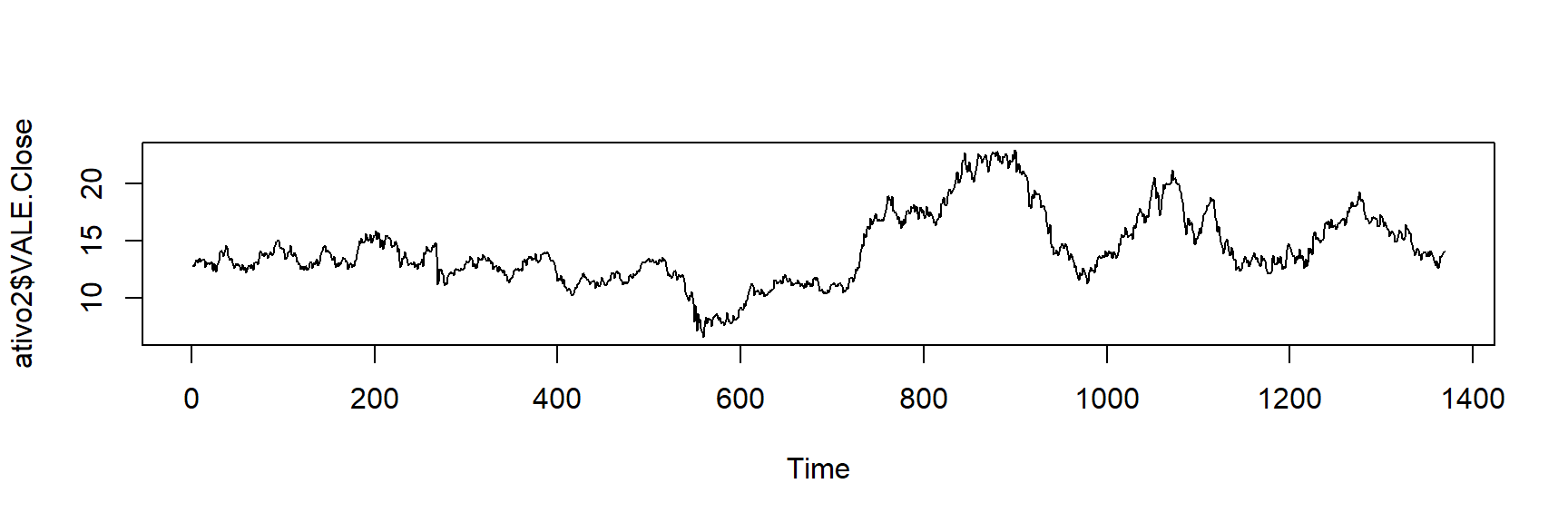

plot.ts(ativo2$VALE.Close) # Serie temporal de valor de fechamento da VALE

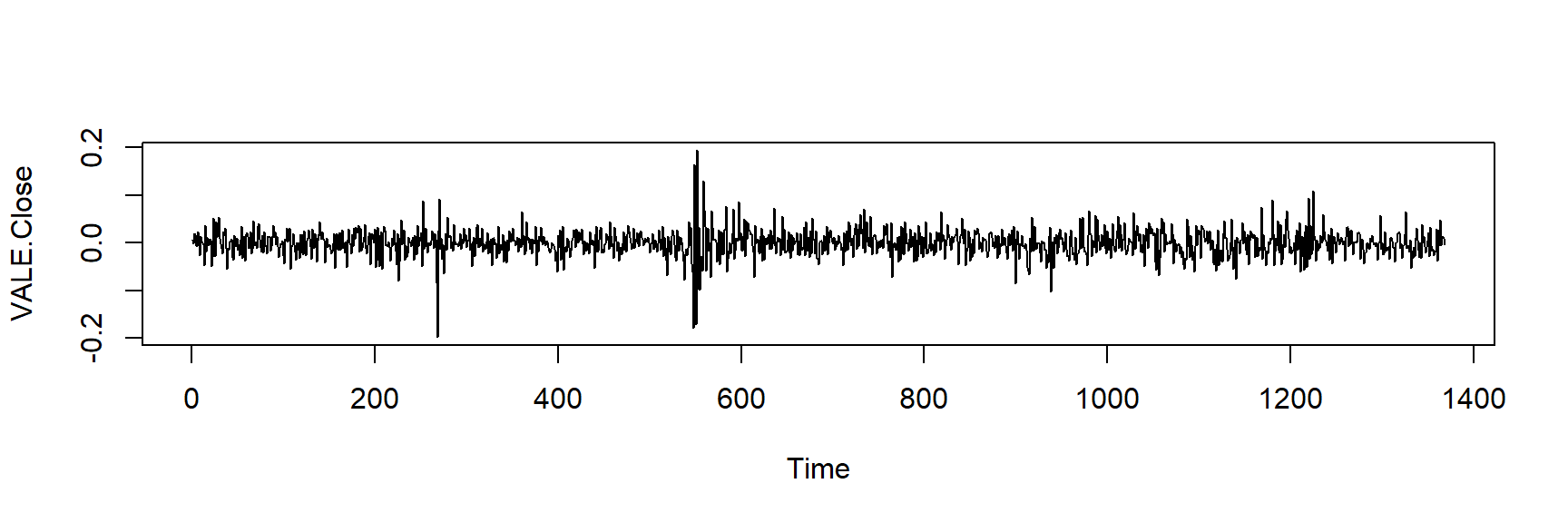

plot.ts(rTS) # Serie de retornos logaritmizados da VALE

Então obtemos os valores de estimativas dos parâmetros da regressão:

VALE.media <- dynlm(rTS~1)

| Dependent variable: | |

| rTS | |

| Constant | 0.0001 |

| (0.001) | |

| Observations | 1,368 |

| R2 | 0.000 |

| Adjusted R2 | 0.000 |

| Note: | p<0.1; p<0.05; p<0.01 |

ehatsq <- ts(resid(VALE.media)^2) # Obtenho os valores da serie de residuos do modelo ARCH elevado ao quadrado

VALE.ARCH <- dynlm(ehatsq~L(ehatsq)) # Agora estimo o modelo dinamico usando a serie de residuos

summary(VALE.ARCH) # Printa os resultados

Time series regression with "ts" data:

Start = 2, End = 1368

Call:

dynlm(formula = ehatsq ~ L(ehatsq))

Residuals:

Min 1Q Median 3Q Max

-0.016531 -0.000548 -0.000380 0.000108 0.035992

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 4.591e-04 6.108e-05 7.517 1.01e-13 ***

L(ehatsq) 4.227e-01 2.453e-02 17.234 < 2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.00214 on 1365 degrees of freedom

Multiple R-squared: 0.1787, Adjusted R-squared: 0.1781

F-statistic: 297 on 1 and 1365 DF, p-value: < 2.2e-16

| Dependent variable: | |

| ehatsq | |

| Constant | 0.0005*** |

| (0.0001) | |

| L(ehatsq) | 0.423*** |

| (0.025) | |

| Observations | 1,367 |

| R2 | 0.179 |

| Adjusted R2 | 0.178 |

| Note: | p<0.1; p<0.05; p<0.01 |

library(broom)

T <- nobs(VALE.media)

q <- length(coef(VALE.ARCH))-1

Rsq <- glance(VALE.ARCH)[[1]]

LM <- (T-q)*Rsq

alpha <- 0.05

quiquadr <- qchisq(1-alpha, q)O valor da estatística LM é de 244.3 que deve ser comparado ao valor crítico do qui-quadrado com \(\alpha = 0,05\) e \(q=\) 1 grau de liberdade; este valor é \(\chi^{2}_{(0,95,\,\, 1)}\) = 3.84; isso indica que a hipótese nula é rejeitada, concluindo que a série tem efeitos ARCH.

A mesma conclusão pode ser alcançada se, em vez do procedimento passo a passo, usarmos um dos recursos de teste ARCH do R, a função ArchTest() no pacote FinTS.

library(FinTS)

VALEArchTest <- ArchTest(dlnVALEclose, lags=1, demean=TRUE)

VALEArchTest

ARCH LM-test; Null hypothesis: no ARCH effects

data: dlnVALEclose

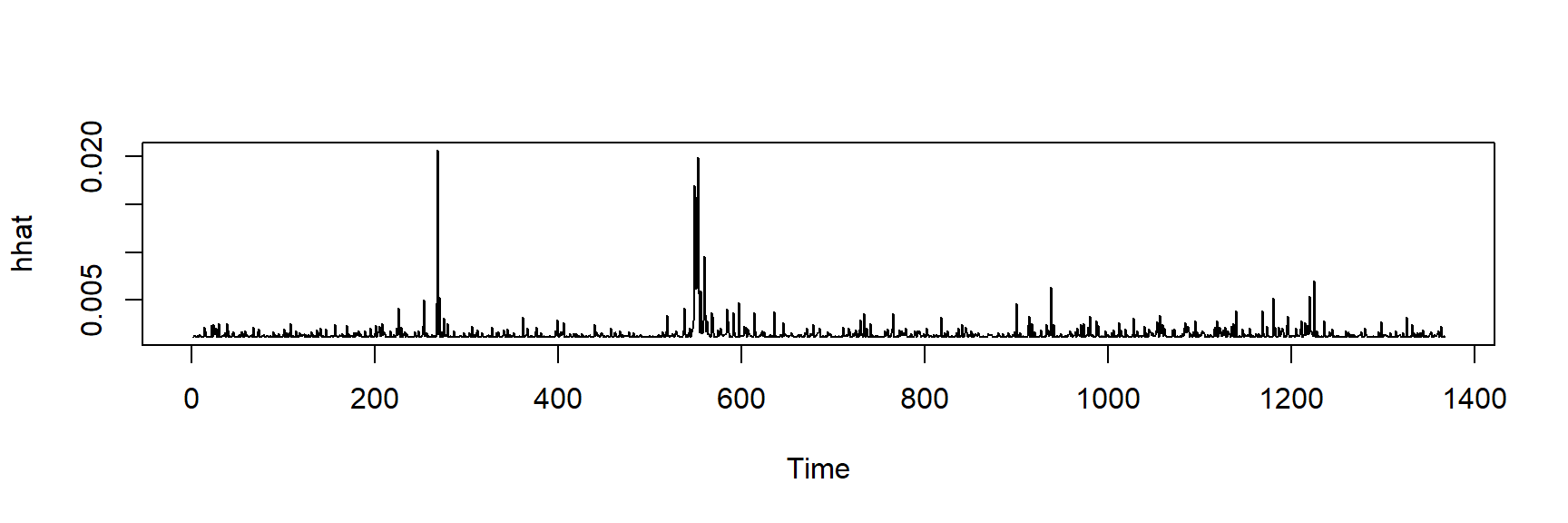

Chi-squared = 244.3, df = 1, p-value < 2.2e-16A função garch() no pacote tseries torna-se um modelo ARCH quando usada com o order = argumento igual a c(0,1). Essa função pode ser usada para estimar e plotar a variância \(h_{t}\) definida na Equação 3, conforme mostrado no código a seguir e na Figura abaixo.

library(tseries)

rTS<-rTS%>%

na.omit() # Retiro os NAs da serie

VALE.arch <- garch(rTS,c(0,1))

***** ESTIMATION WITH ANALYTICAL GRADIENT *****

I INITIAL X(I) D(I)

1 7.555777e-04 1.000e+00

2 5.000000e-02 1.000e+00

IT NF F RELDF PRELDF RELDX STPPAR D*STEP NPRELDF

0 1 -4.247e+03

1 6 -4.252e+03 9.97e-04 2.18e-03 1.0e-03 9.3e+08 1.0e-04 1.01e+06

2 7 -4.252e+03 3.77e-05 4.69e-05 9.9e-04 2.0e+00 1.0e-04 3.39e+01

3 13 -4.271e+03 4.53e-03 7.62e-03 3.8e-01 2.0e+00 6.1e-02 3.38e+01

4 15 -4.273e+03 4.84e-04 1.16e-03 7.8e-02 1.1e+00 1.9e-02 1.85e-03

5 17 -4.279e+03 1.25e-03 8.55e-04 1.2e-01 0.0e+00 3.7e-02 8.55e-04

6 18 -4.281e+03 4.69e-04 4.06e-04 1.0e-01 1.8e-01 3.7e-02 4.15e-04

7 19 -4.281e+03 1.54e-04 1.17e-04 6.3e-02 0.0e+00 2.8e-02 1.17e-04

8 20 -4.281e+03 2.52e-05 2.17e-05 2.9e-02 0.0e+00 1.4e-02 2.17e-05

9 21 -4.281e+03 9.45e-07 8.79e-07 6.5e-03 0.0e+00 3.2e-03 8.79e-07

10 22 -4.281e+03 6.37e-09 6.26e-09 5.8e-04 0.0e+00 2.9e-04 6.26e-09

11 23 -4.281e+03 2.56e-12 2.53e-12 1.1e-05 0.0e+00 5.4e-06 2.53e-12

***** RELATIVE FUNCTION CONVERGENCE *****

FUNCTION -4.281430e+03 RELDX 1.083e-05

FUNC. EVALS 23 GRAD. EVALS 12

PRELDF 2.526e-12 NPRELDF 2.526e-12

I FINAL X(I) D(I) G(I)

1 5.627445e-04 1.000e+00 1.828e-01

2 2.475817e-01 1.000e+00 4.131e-05sbydarch <- summary(VALE.arch)

sbydarch

Call:

garch(x = rTS, order = c(0, 1))

Model:

GARCH(0,1)

Residuals:

Min 1Q Median 3Q Max

-4.68465 -0.59037 0.02321 0.59399 4.37563

Coefficient(s):

Estimate Std. Error t value Pr(>|t|)

a0 5.627e-04 2.198e-05 25.6 <2e-16 ***

a1 2.476e-01 2.293e-02 10.8 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Diagnostic Tests:

Jarque Bera Test

data: Residuals

X-squared = 134.77, df = 2, p-value < 2.2e-16

Box-Ljung test

data: Squared.Residuals

X-squared = 0.024545, df = 1, p-value = 0.8755hhat <- ts(2*VALE.arch$fitted.values[-1,1]^2)

plot.ts(hhat)

O modelo GARCH

library(rugarch)

garchSpec <- ugarchspec(

variance.model=list(model="sGARCH",

garchOrder=c(1,1)),

mean.model=list(armaOrder=c(0,0)),

distribution.model="std")

garchFit <- ugarchfit(spec=garchSpec, data=rTS)

coef(garchFit) mu omega alpha1 beta1 shape

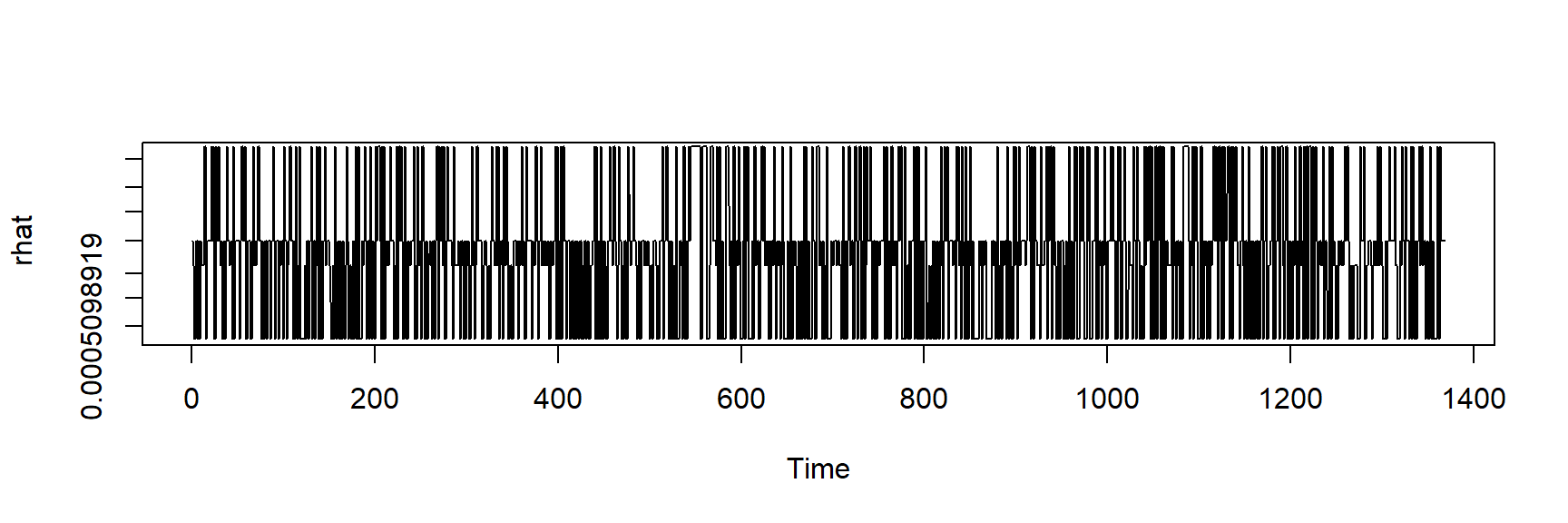

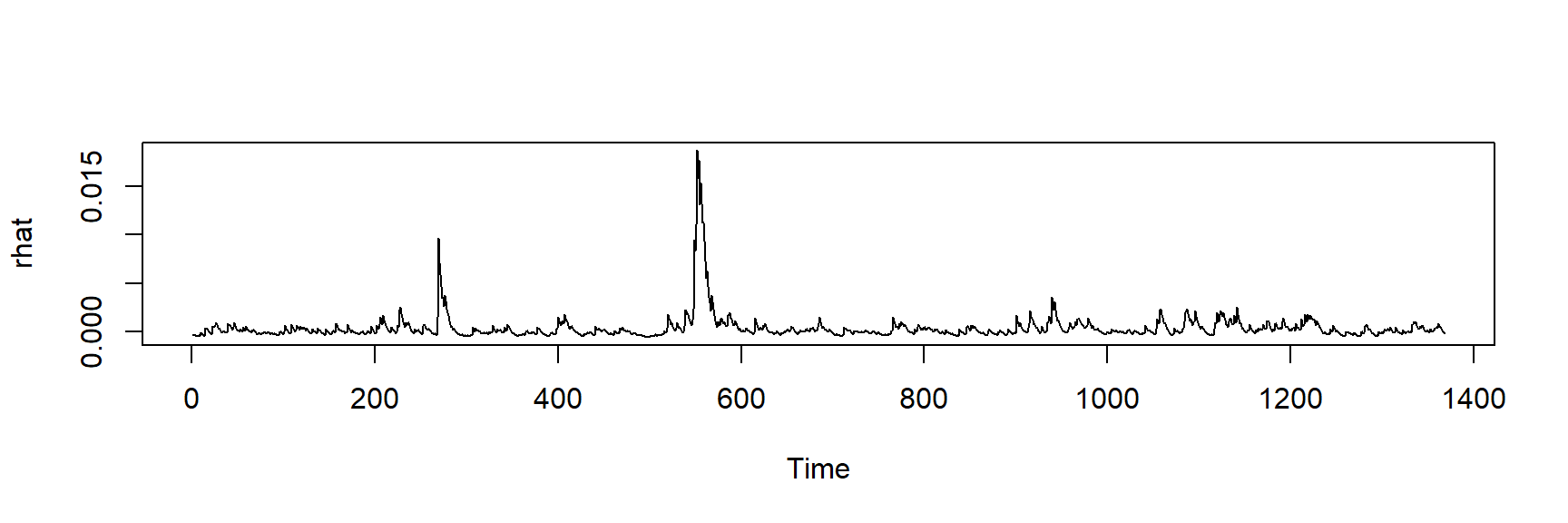

5.098919e-04 8.181086e-05 7.732878e-02 8.075895e-01 6.563801e+00 rhat <- garchFit@fit$fitted.values

plot.ts(rhat)

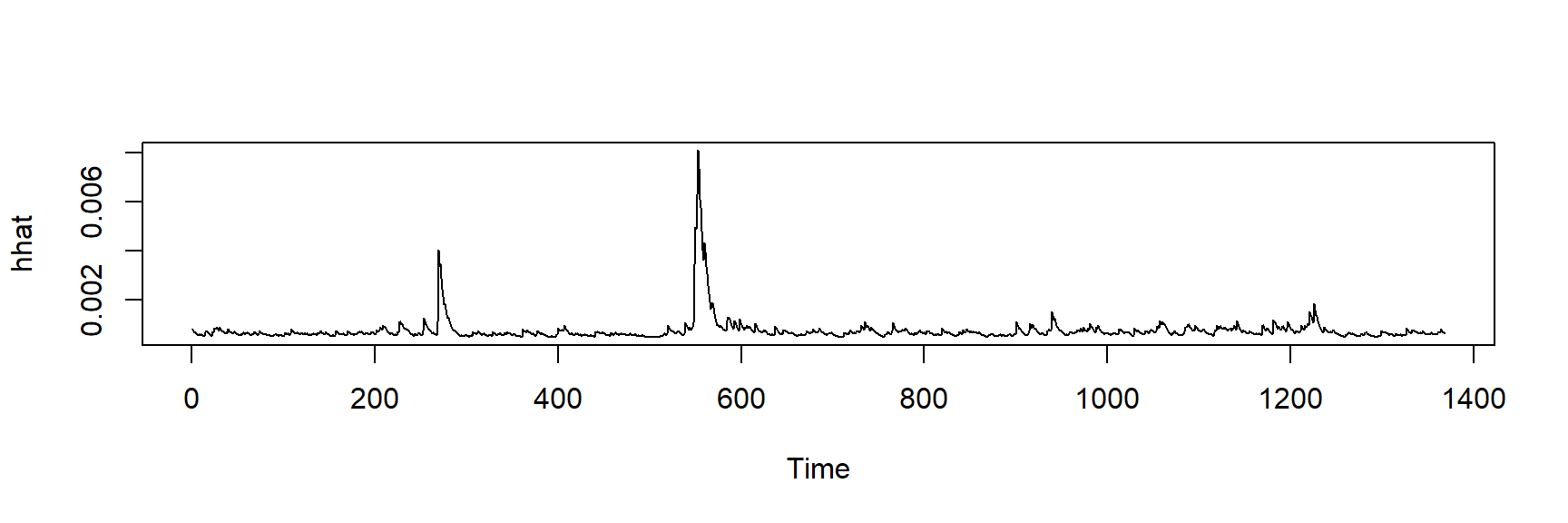

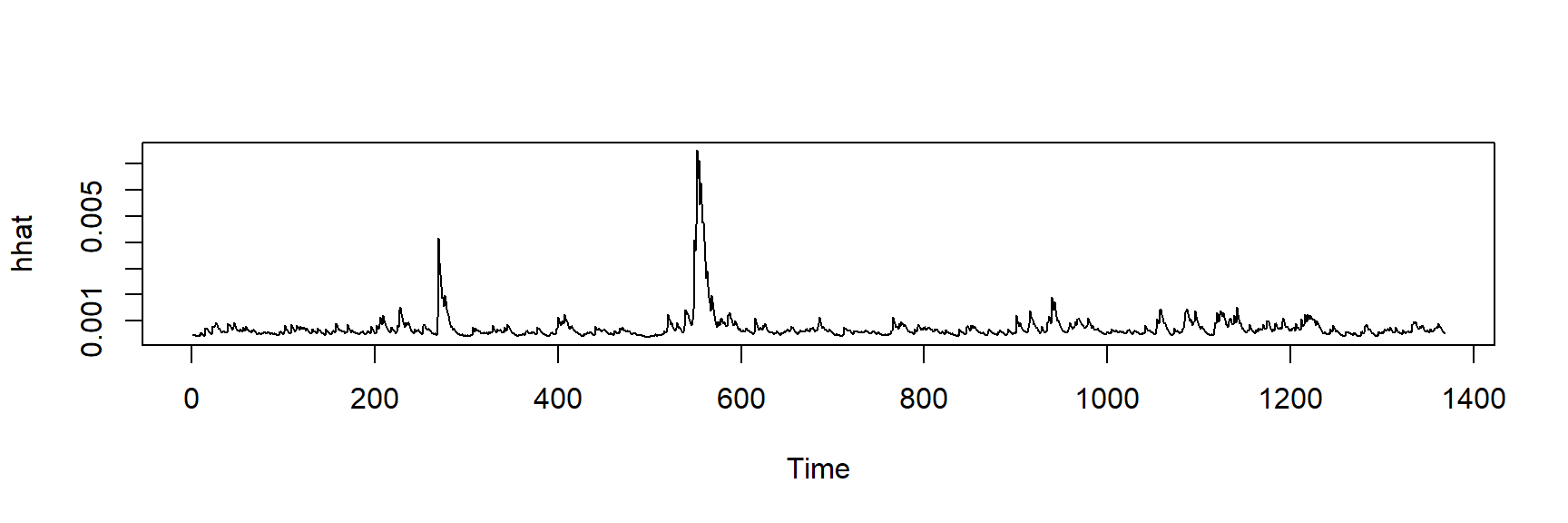

hhat <- ts(garchFit@fit$sigma^2)

plot.ts(hhat)

# tGARCH

garchMod <- ugarchspec(variance.model=list(model="fGARCH",

garchOrder=c(1,1),

submodel="TGARCH"),

mean.model=list(armaOrder=c(0,0)),

distribution.model="std")

garchFit <- ugarchfit(spec=garchMod, data=rTS)

coef(garchFit) mu omega alpha1 beta1 eta11 shape

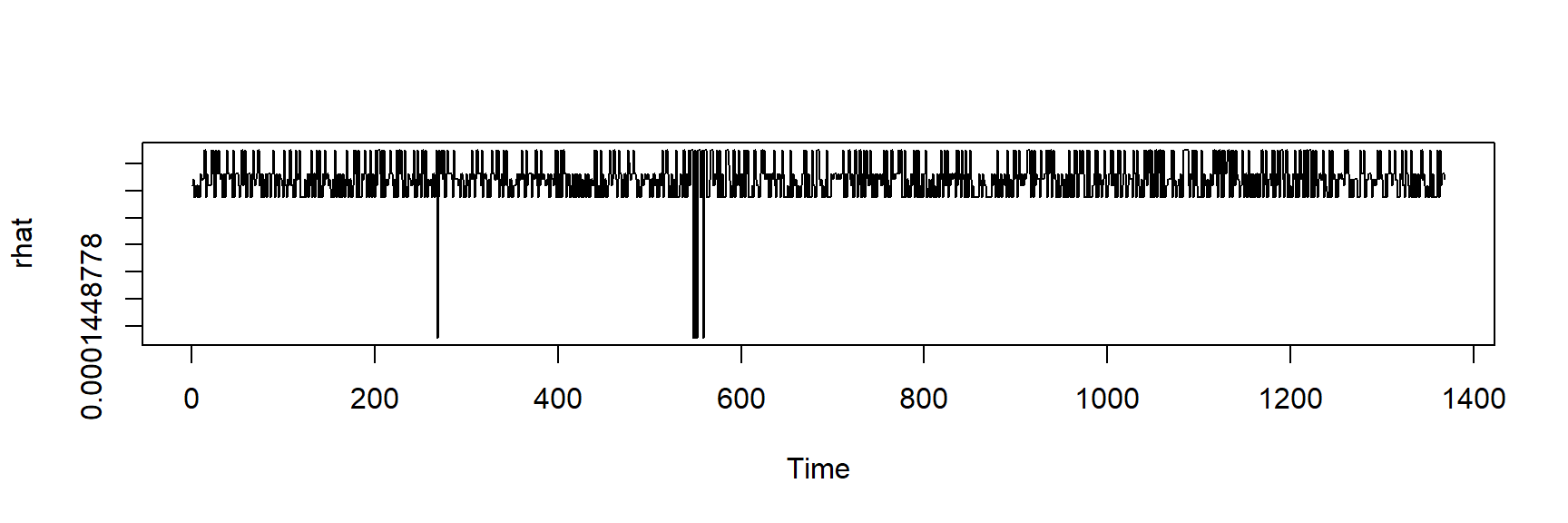

0.0001448778 0.0024951666 0.0829903566 0.8426163519 0.6037352495 6.7955576554 rhat <- garchFit@fit$fitted.values

plot.ts(rhat)

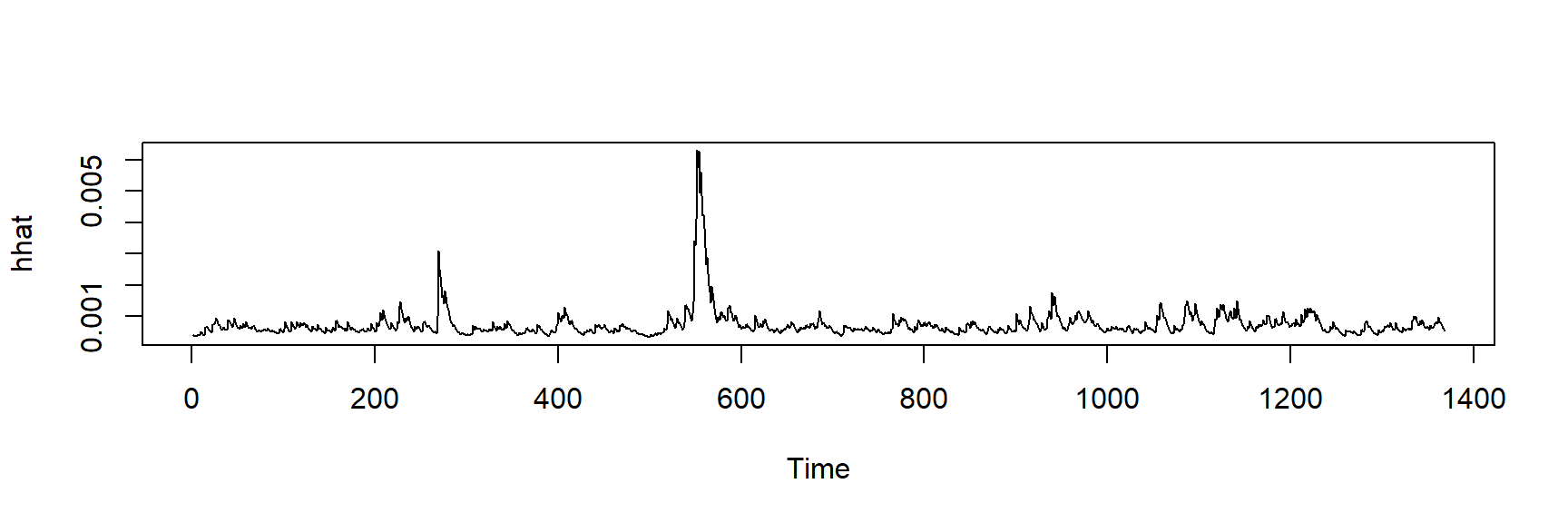

hhat <- ts(garchFit@fit$sigma^2)

plot.ts(hhat)

# GARCH-in-mean

garchMod <- ugarchspec(

variance.model=list(model="fGARCH",

garchOrder=c(1,1),

submodel="APARCH"),

mean.model=list(armaOrder=c(0,0),

include.mean=TRUE,

archm=TRUE,

archpow=2

),

distribution.model="std"

)

garchFit <- ugarchfit(spec=garchMod, data=rTS)

coef(garchFit) mu archm omega alpha1 beta1 eta11

-0.001572400 2.693463496 0.001299905 0.083006027 0.814291951 0.578064680

lambda shape

1.237831744 6.936388133 rhat <- garchFit@fit$fitted.values

plot.ts(rhat)

hhat <- ts(garchFit@fit$sigma^2)

plot.ts(hhat)

As Figuras anteriores mostram algumas versões do modelo GARCH. As previsões podem ser obtidas usando a função ugarchboot() do pacote ugarch.

Outro script para a News Impact Curve

library(PerformanceAnalytics)

library(quantmod)

library(rugarch)

library(car)

library(FinTS)options(digits=4)

VALEfechamento<-ativo2$VALE.Close

# Calcula o log retorno dos precos de fechamento da VALE

VALE.ret = CalculateReturns(VALEfechamento, method="log")

VALE.ret[1:10,] # printa as primeiras dez linhas VALE.Close

2018-01-02 NA

2018-01-03 0.006245

2018-01-04 -0.001558

2018-01-05 0.020062

2018-01-08 0.017418

2018-01-09 -0.006024

2018-01-10 -0.006821

2018-01-11 0.022557

2018-01-12 0.005930

2018-01-16 -0.026968VALE.ret=VALE.ret[-1,] # Removo o primeiro NA

VALE.ret[1:10,] # printa as primeiras dez linhas VALE.Close

2018-01-03 0.006245

2018-01-04 -0.001558

2018-01-05 0.020062

2018-01-08 0.017418

2018-01-09 -0.006024

2018-01-10 -0.006821

2018-01-11 0.022557

2018-01-12 0.005930

2018-01-16 -0.026968

2018-01-17 0.013575GARCH Assimétrico

Agora vamos definir o GARCH assimétrico

garch11.spec = ugarchspec(variance.model = list(garchOrder=c(1,1)),

mean.model = list(armaOrder=c(0,0)))

VALE.garch11.fit = ugarchfit(spec=garch11.spec, data=VALE.ret,

solver.control=list(trace = 1))

Iter: 1 fn: -3045.0634 Pars: 0.0005617 0.0001112 0.1226330 0.7247662

Iter: 2 fn: -3045.0634 Pars: 0.0005616 0.0001112 0.1226429 0.7247721

solnp--> Completed in 2 iterationsVALE.garch11.fit

*---------------------------------*

* GARCH Model Fit *

*---------------------------------*

Conditional Variance Dynamics

-----------------------------------

GARCH Model : sGARCH(1,1)

Mean Model : ARFIMA(0,0,0)

Distribution : norm

Optimal Parameters

------------------------------------

Estimate Std. Error t value Pr(>|t|)

mu 0.000562 0.000676 0.83051 0.406253

omega 0.000111 0.000034 3.27136 0.001070

alpha1 0.122643 0.024780 4.94933 0.000001

beta1 0.724772 0.063199 11.46801 0.000000

Robust Standard Errors:

Estimate Std. Error t value Pr(>|t|)

mu 0.000562 0.000667 0.84239 0.399568

omega 0.000111 0.000060 1.84512 0.065019

alpha1 0.122643 0.059972 2.04499 0.040856

beta1 0.724772 0.124365 5.82780 0.000000

LogLikelihood : 3045

Information Criteria

------------------------------------

Akaike -4.4460

Bayes -4.4307

Shibata -4.4460

Hannan-Quinn -4.4403

Weighted Ljung-Box Test on Standardized Residuals

------------------------------------

statistic p-value

Lag[1] 0.01975 0.8882

Lag[2*(p+q)+(p+q)-1][2] 0.23233 0.8346

Lag[4*(p+q)+(p+q)-1][5] 1.50811 0.7379

d.o.f=0

H0 : No serial correlation

Weighted Ljung-Box Test on Standardized Squared Residuals

------------------------------------

statistic p-value

Lag[1] 6.808 0.009077

Lag[2*(p+q)+(p+q)-1][5] 7.745 0.034073

Lag[4*(p+q)+(p+q)-1][9] 9.341 0.069102

d.o.f=2

Weighted ARCH LM Tests

------------------------------------

Statistic Shape Scale P-Value

ARCH Lag[3] 0.090 0.500 2.000 0.7642

ARCH Lag[5] 1.151 1.440 1.667 0.6888

ARCH Lag[7] 1.996 2.315 1.543 0.7181

Nyblom stability test

------------------------------------

Joint Statistic: 0.6963

Individual Statistics:

mu 0.05934

omega 0.17910

alpha1 0.07439

beta1 0.20613

Asymptotic Critical Values (10% 5% 1%)

Joint Statistic: 1.07 1.24 1.6

Individual Statistic: 0.35 0.47 0.75

Sign Bias Test

------------------------------------

t-value prob sig

Sign Bias 1.1389 0.254925

Negative Sign Bias 3.1327 0.001769 ***

Positive Sign Bias 0.8256 0.409155

Joint Effect 12.0285 0.007286 ***

Adjusted Pearson Goodness-of-Fit Test:

------------------------------------

group statistic p-value(g-1)

1 20 38.67 0.004877

2 30 43.18 0.043775

3 40 57.32 0.029368

4 50 72.64 0.015750

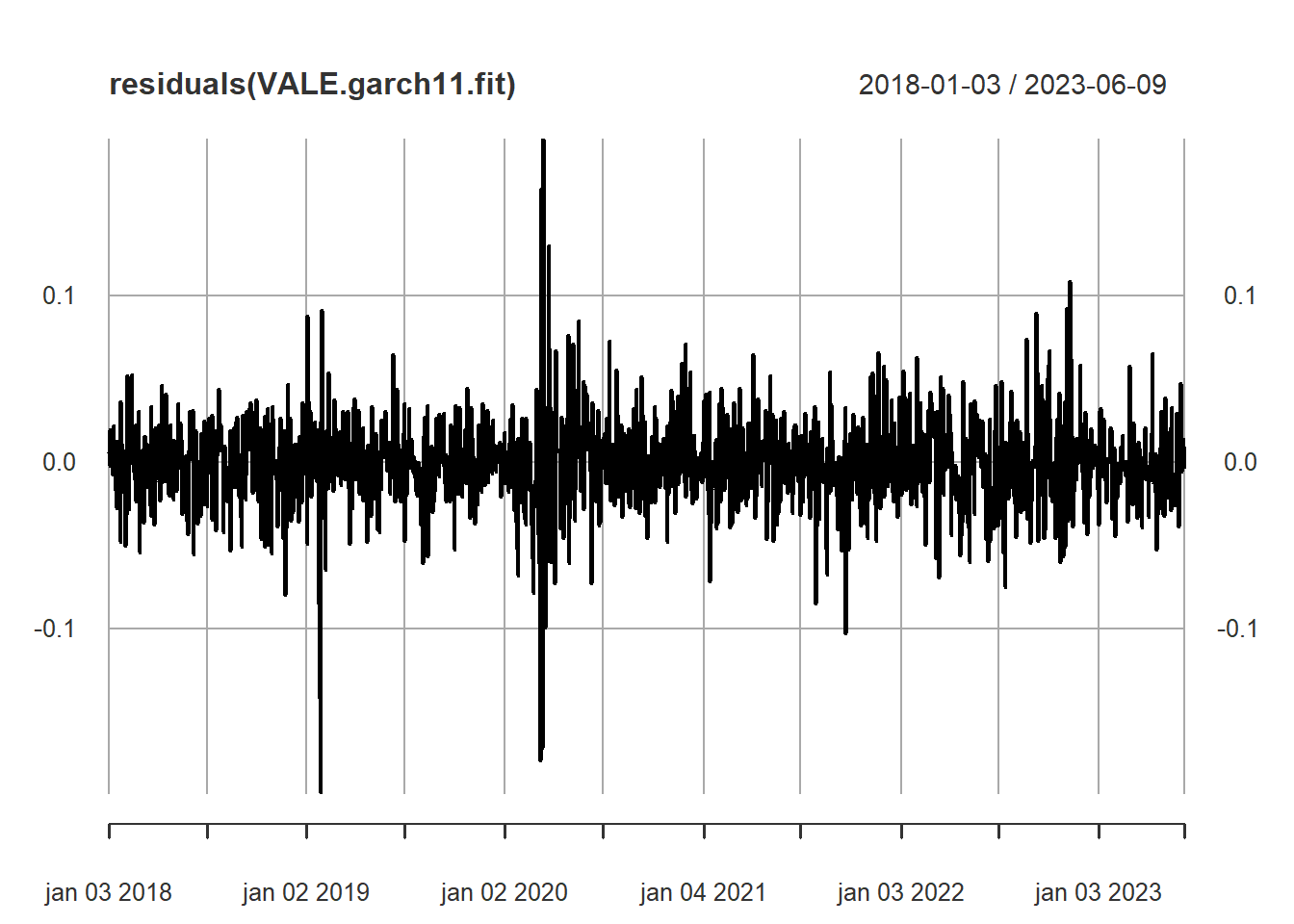

Elapsed time : 0.1835 plot(residuals(VALE.garch11.fit))

Rodaremos o teste de Engle & NG. para o viés de sinal:

O teste de viés de sinal considera a variável \(S_{t-1}^{-}\), uma variável fictícia que assume o valor um quando \(\epsilon_{t-1}\) é negativo e zero, caso contrário. Este teste examina o impacto de choques de retorno positivo e negativo sobre a volatilidade não prevista pelo modelo em consideração. O teste de viés de tamanho negativo utiliza a variável \(S_{t-1}^{-}\) \(\epsilon_{t-1}\). Ele se concentra nos diferentes efeitos que grandes e pequenos choques de retorno negativo têm sobre a volatilidade, o que não é previsto pelo modelo de volatilidade. O teste de viés de tamanho positivo utiliza a variável \(S_{t-1}^{+}\) \(\epsilon_{t-1}\) onde \(S_{t-1}^{+}\) é definido como 1 menos \(S_{t-1}\). Ele se concentra nos diferentes impactos que grandes e pequenos choques de retorno positivo podem ter sobre a volatilidade, que não são explicados pelo modelo de volatilidade.

signbias(VALE.garch11.fit) t-value prob sig

Sign Bias 1.1389 0.254925

Negative Sign Bias 3.1327 0.001769 ***

Positive Sign Bias 0.8256 0.409155

Joint Effect 12.0285 0.007286 ***Como apontado acima, o efeito de viés de negativo foi o que apresentou significância.

Modelo EGARCH de Nelson

egarch11.spec = ugarchspec(variance.model=list(model="eGARCH",

garchOrder=c(1,1)),

mean.model=list(armaOrder=c(0,0)))

VALE.egarch11.fit = ugarchfit(egarch11.spec, VALE.ret)

VALE.egarch11.fit

*---------------------------------*

* GARCH Model Fit *

*---------------------------------*

Conditional Variance Dynamics

-----------------------------------

GARCH Model : eGARCH(1,1)

Mean Model : ARFIMA(0,0,0)

Distribution : norm

Optimal Parameters

------------------------------------

Estimate Std. Error t value Pr(>|t|)

mu -0.000209 0.000671 -0.31211 0.754954

omega -0.944470 0.262859 -3.59307 0.000327

alpha1 -0.132769 0.027603 -4.80997 0.000002

beta1 0.869359 0.036082 24.09385 0.000000

gamma1 0.213962 0.035379 6.04777 0.000000

Robust Standard Errors:

Estimate Std. Error t value Pr(>|t|)

mu -0.000209 0.000705 -0.2969 0.766544

omega -0.944470 0.573335 -1.6473 0.099491

alpha1 -0.132769 0.059557 -2.2293 0.025796

beta1 0.869359 0.079300 10.9629 0.000000

gamma1 0.213962 0.076979 2.7795 0.005445

LogLikelihood : 3054

Information Criteria

------------------------------------

Akaike -4.4573

Bayes -4.4382

Shibata -4.4573

Hannan-Quinn -4.4501

Weighted Ljung-Box Test on Standardized Residuals

------------------------------------

statistic p-value

Lag[1] 3.039e-06 0.9986

Lag[2*(p+q)+(p+q)-1][2] 1.742e-01 0.8703

Lag[4*(p+q)+(p+q)-1][5] 1.226e+00 0.8068

d.o.f=0

H0 : No serial correlation

Weighted Ljung-Box Test on Standardized Squared Residuals

------------------------------------

statistic p-value

Lag[1] 6.503 0.01077

Lag[2*(p+q)+(p+q)-1][5] 6.939 0.05367

Lag[4*(p+q)+(p+q)-1][9] 8.567 0.09955

d.o.f=2

Weighted ARCH LM Tests

------------------------------------

Statistic Shape Scale P-Value

ARCH Lag[3] 0.09855 0.500 2.000 0.7536

ARCH Lag[5] 0.49815 1.440 1.667 0.8842

ARCH Lag[7] 1.95431 2.315 1.543 0.7270

Nyblom stability test

------------------------------------

Joint Statistic: 0.8103

Individual Statistics:

mu 0.1289

omega 0.1249

alpha1 0.1322

beta1 0.1188

gamma1 0.2905

Asymptotic Critical Values (10% 5% 1%)

Joint Statistic: 1.28 1.47 1.88

Individual Statistic: 0.35 0.47 0.75

Sign Bias Test

------------------------------------

t-value prob sig

Sign Bias 1.19739 0.23136

Negative Sign Bias 2.22994 0.02591 **

Positive Sign Bias 0.05336 0.95745

Joint Effect 4.99000 0.17253

Adjusted Pearson Goodness-of-Fit Test:

------------------------------------

group statistic p-value(g-1)

1 20 33.23 0.02262

2 30 44.98 0.02954

3 40 50.36 0.10506

4 50 69.35 0.02935

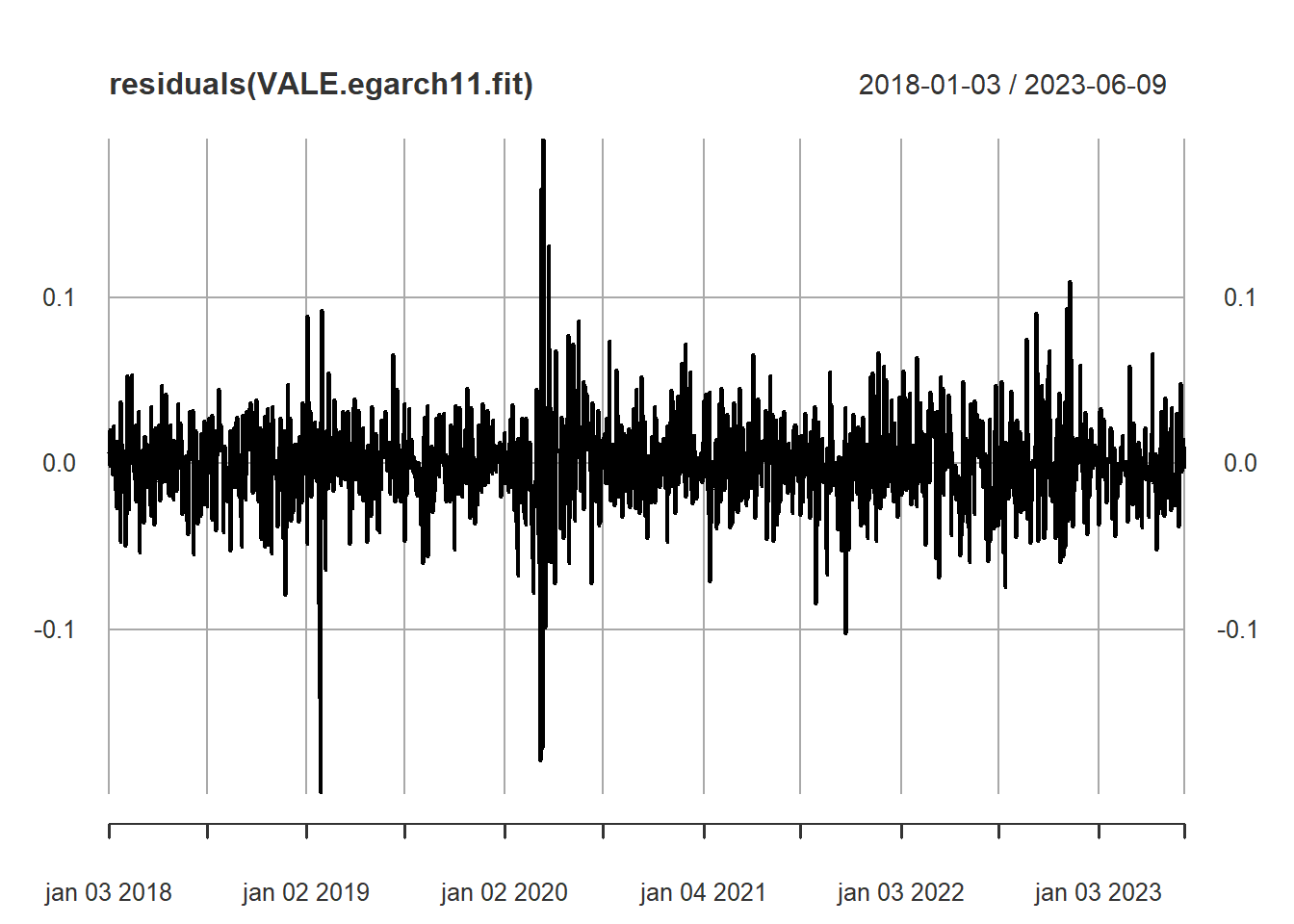

Elapsed time : 0.1737 plot(residuals(VALE.egarch11.fit))

Modelo GJR GARCH

gjrgarch11.spec = ugarchspec(variance.model=list(model="gjrGARCH",

garchOrder=c(1,1)),

mean.model=list(armaOrder=c(0,0)))

VALE.gjrgarch11.fit = ugarchfit(gjrgarch11.spec, VALE.ret)

VALE.gjrgarch11.fit

*---------------------------------*

* GARCH Model Fit *

*---------------------------------*

Conditional Variance Dynamics

-----------------------------------

GARCH Model : gjrGARCH(1,1)

Mean Model : ARFIMA(0,0,0)

Distribution : norm

Optimal Parameters

------------------------------------

Estimate Std. Error t value Pr(>|t|)

mu 0.000047 0.000677 0.068915 0.945057

omega 0.000128 0.000032 4.002958 0.000063

alpha1 0.013622 0.021287 0.639913 0.522229

beta1 0.711888 0.056802 12.532797 0.000000

gamma1 0.192620 0.046233 4.166272 0.000031

Robust Standard Errors:

Estimate Std. Error t value Pr(>|t|)

mu 0.000047 0.000702 0.06647 0.947004

omega 0.000128 0.000056 2.29011 0.022015

alpha1 0.013622 0.021603 0.63055 0.528333

beta1 0.711888 0.102368 6.95423 0.000000

gamma1 0.192620 0.094309 2.04243 0.041109

LogLikelihood : 3057

Information Criteria

------------------------------------

Akaike -4.4618

Bayes -4.4427

Shibata -4.4618

Hannan-Quinn -4.4547

Weighted Ljung-Box Test on Standardized Residuals

------------------------------------

statistic p-value

Lag[1] 0.007495 0.9310

Lag[2*(p+q)+(p+q)-1][2] 0.098210 0.9209

Lag[4*(p+q)+(p+q)-1][5] 1.211921 0.8101

d.o.f=0

H0 : No serial correlation

Weighted Ljung-Box Test on Standardized Squared Residuals

------------------------------------

statistic p-value

Lag[1] 3.171 0.07496

Lag[2*(p+q)+(p+q)-1][5] 4.090 0.24311

Lag[4*(p+q)+(p+q)-1][9] 6.367 0.25817

d.o.f=2

Weighted ARCH LM Tests

------------------------------------

Statistic Shape Scale P-Value

ARCH Lag[3] 0.2943 0.500 2.000 0.5875

ARCH Lag[5] 1.1262 1.440 1.667 0.6959

ARCH Lag[7] 3.0940 2.315 1.543 0.4960

Nyblom stability test

------------------------------------

Joint Statistic: 0.9498

Individual Statistics:

mu 0.1273

omega 0.2589

alpha1 0.1830

beta1 0.3513

gamma1 0.1092

Asymptotic Critical Values (10% 5% 1%)

Joint Statistic: 1.28 1.47 1.88

Individual Statistic: 0.35 0.47 0.75

Sign Bias Test

------------------------------------

t-value prob sig

Sign Bias 0.6108 0.5414

Negative Sign Bias 1.5094 0.1314

Positive Sign Bias 0.2721 0.7856

Joint Effect 2.3523 0.5026

Adjusted Pearson Goodness-of-Fit Test:

------------------------------------

group statistic p-value(g-1)

1 20 33.81 0.01933

2 30 39.41 0.09401

3 40 49.37 0.12351

4 50 64.75 0.06522

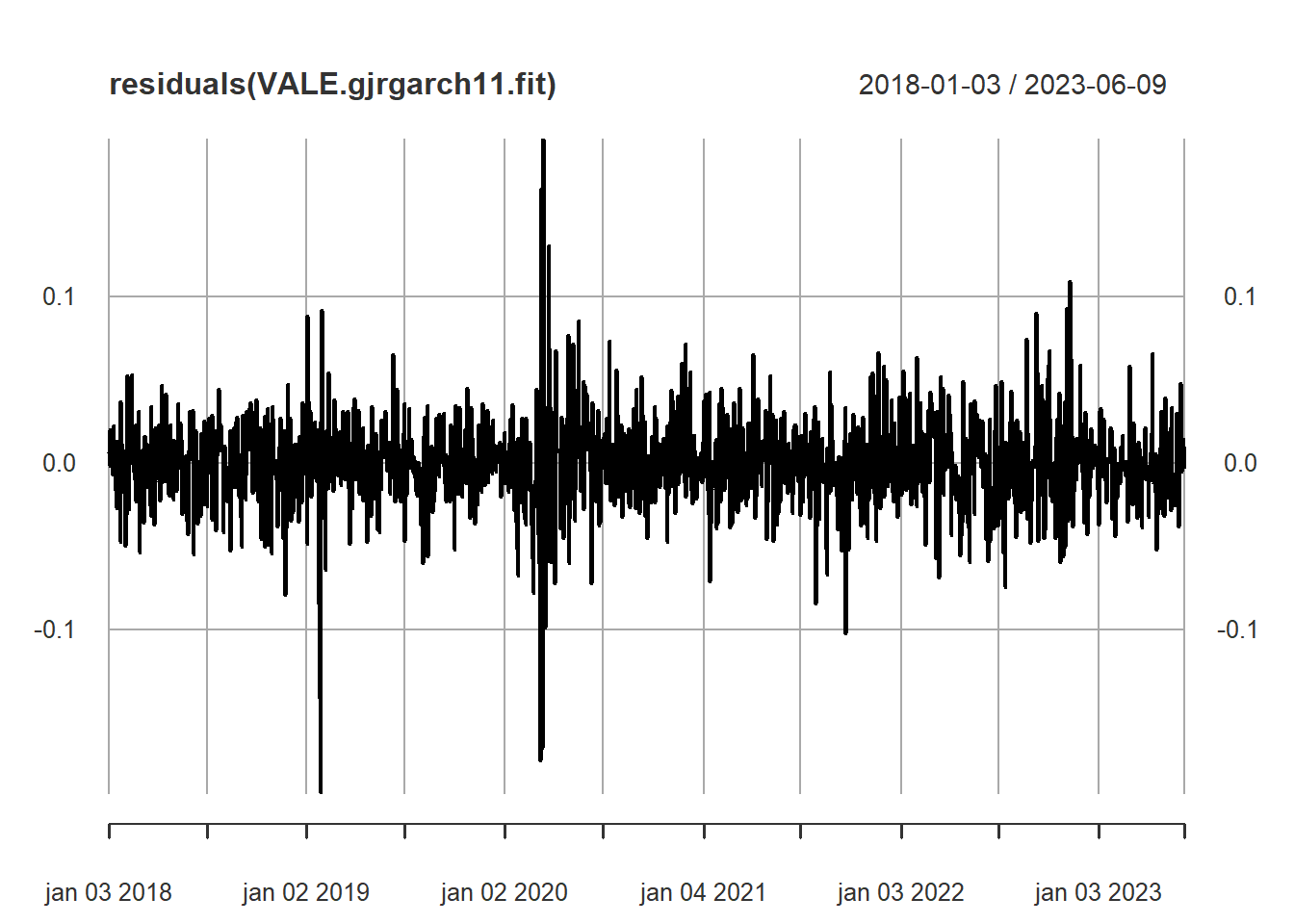

Elapsed time : 0.3573 plot(residuals(VALE.gjrgarch11.fit))

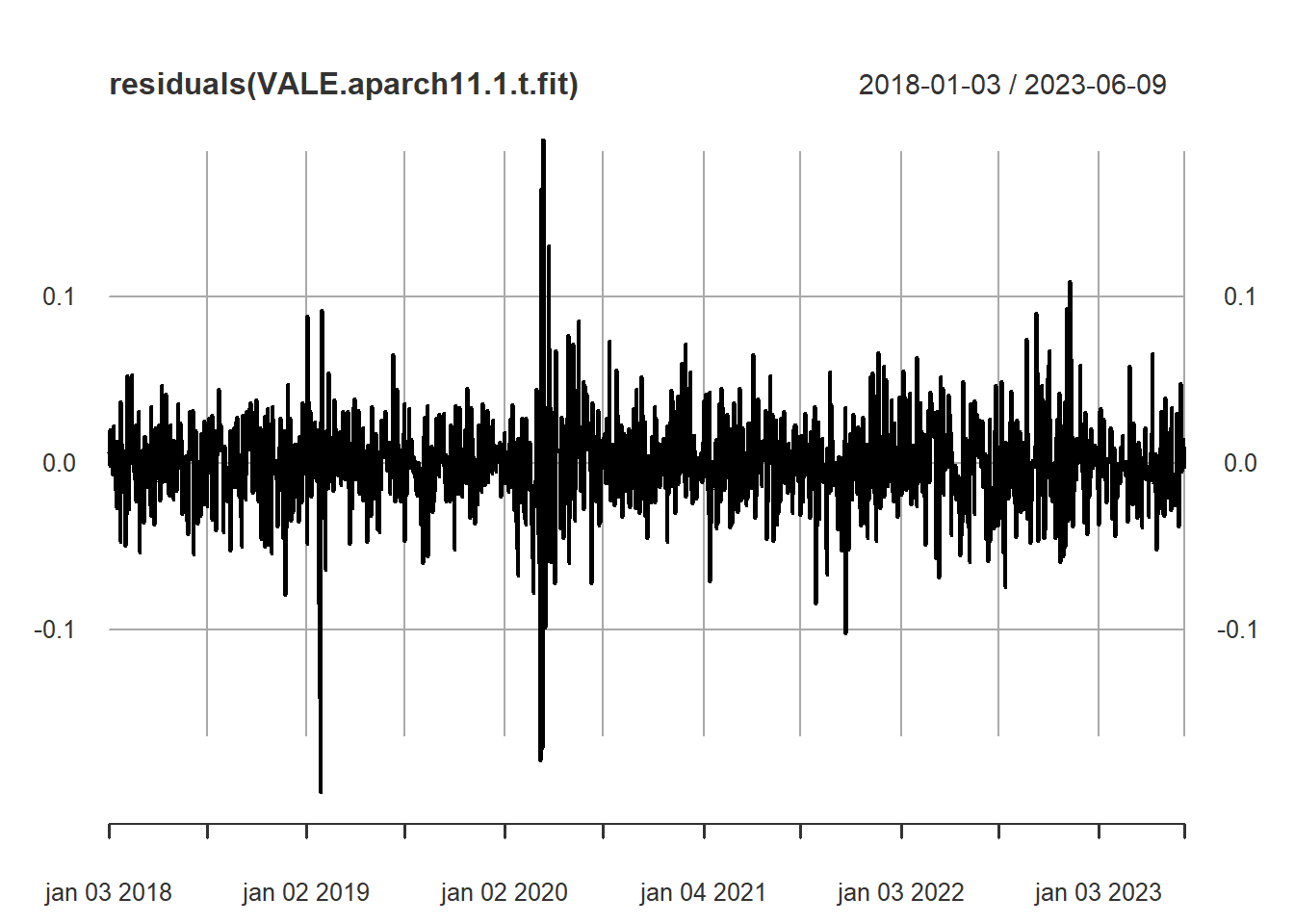

Modelo APARCH

aparch11.1.spec = ugarchspec(variance.model=list(model="apARCH",

garchOrder=c(1,1)),

mean.model=list(armaOrder=c(0,0)),

fixed.pars=list(delta=1))

VALE.aparch11.1.fit = ugarchfit(aparch11.1.spec, VALE.ret)

VALE.aparch11.1.fit

*---------------------------------*

* GARCH Model Fit *

*---------------------------------*

Conditional Variance Dynamics

-----------------------------------

GARCH Model : apARCH(1,1)

Mean Model : ARFIMA(0,0,0)

Distribution : norm

Optimal Parameters

------------------------------------

Estimate Std. Error t value Pr(>|t|)

mu -0.000214 0.000673 -0.31766 0.750739

omega 0.004021 0.001095 3.67160 0.000241

alpha1 0.116203 0.020798 5.58731 0.000000

beta1 0.760789 0.051128 14.87997 0.000000

gamma1 0.653656 0.150914 4.33131 0.000015

delta 1.000000 NA NA NA

Robust Standard Errors:

Estimate Std. Error t value Pr(>|t|)

mu -0.000214 0.000703 -0.30417 0.761000

omega 0.004021 0.002296 1.75105 0.079937

alpha1 0.116203 0.042770 2.71689 0.006590

beta1 0.760789 0.112343 6.77204 0.000000

gamma1 0.653656 0.166548 3.92472 0.000087

delta 1.000000 NA NA NA

LogLikelihood : 3054

Information Criteria

------------------------------------

Akaike -4.4573

Bayes -4.4382

Shibata -4.4573

Hannan-Quinn -4.4501

Weighted Ljung-Box Test on Standardized Residuals

------------------------------------

statistic p-value

Lag[1] 0.001546 0.9686

Lag[2*(p+q)+(p+q)-1][2] 0.251705 0.8232

Lag[4*(p+q)+(p+q)-1][5] 1.405315 0.7632

d.o.f=0

H0 : No serial correlation

Weighted Ljung-Box Test on Standardized Squared Residuals

------------------------------------

statistic p-value

Lag[1] 9.593 0.001953

Lag[2*(p+q)+(p+q)-1][5] 9.929 0.009601

Lag[4*(p+q)+(p+q)-1][9] 11.523 0.023244

d.o.f=2

Weighted ARCH LM Tests

------------------------------------

Statistic Shape Scale P-Value

ARCH Lag[3] 0.06548 0.500 2.000 0.7980

ARCH Lag[5] 0.59218 1.440 1.667 0.8561

ARCH Lag[7] 1.97026 2.315 1.543 0.7236

Nyblom stability test

------------------------------------

Joint Statistic: 0.7544

Individual Statistics:

mu 0.13466

omega 0.08956

alpha1 0.09893

beta1 0.10852

gamma1 0.12171

Asymptotic Critical Values (10% 5% 1%)

Joint Statistic: 1.28 1.47 1.88

Individual Statistic: 0.35 0.47 0.75

Sign Bias Test

------------------------------------

t-value prob sig

Sign Bias 1.461350 0.14415

Negative Sign Bias 2.570240 0.01027 **

Positive Sign Bias 0.002776 0.99779

Joint Effect 6.651720 0.08387 *

Adjusted Pearson Goodness-of-Fit Test:

------------------------------------

group statistic p-value(g-1)

1 20 35.42 0.012422

2 30 43.97 0.036913

3 40 50.54 0.102050

4 50 75.06 0.009726

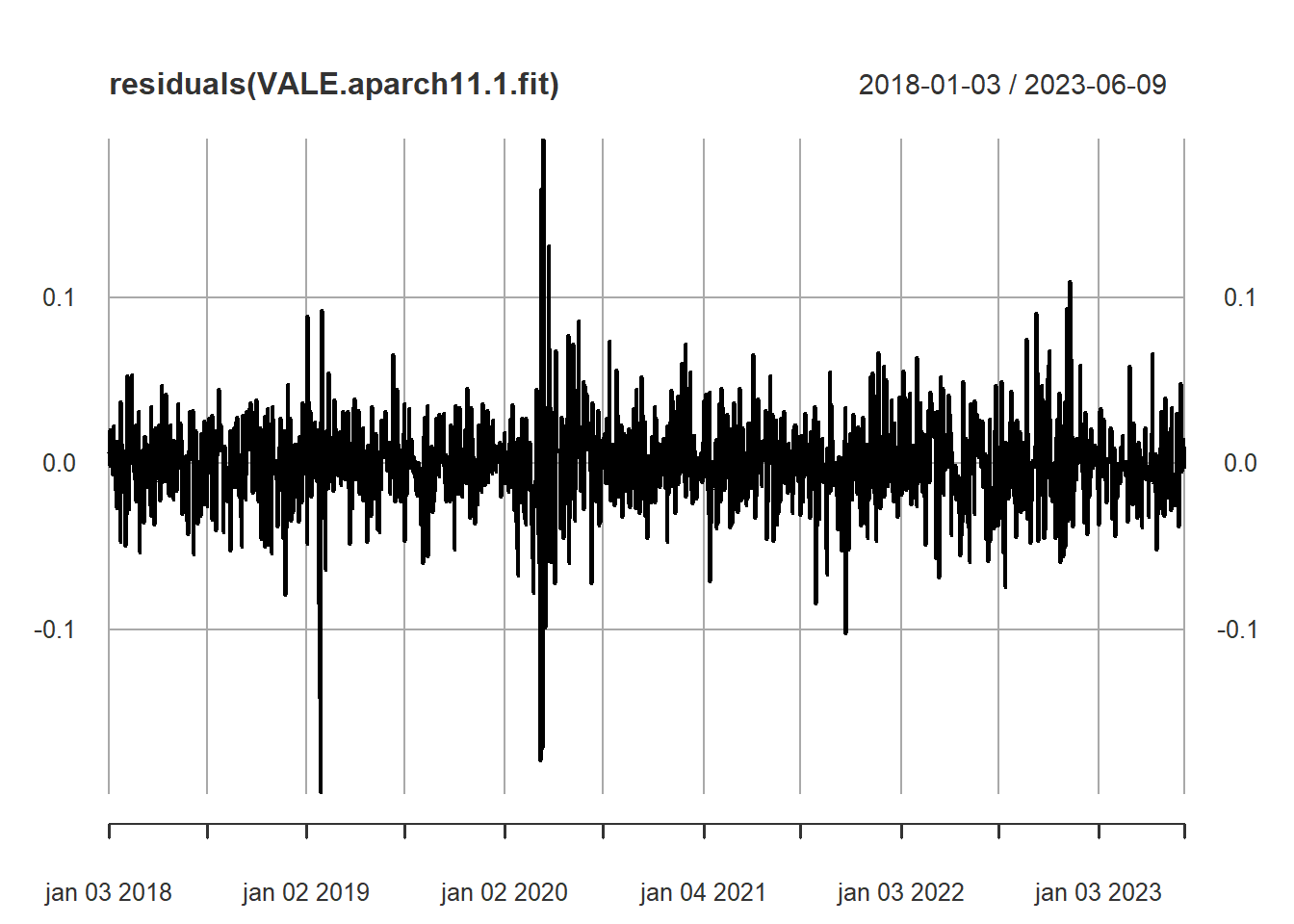

Elapsed time : 0.4172 plot(residuals(VALE.aparch11.1.fit))

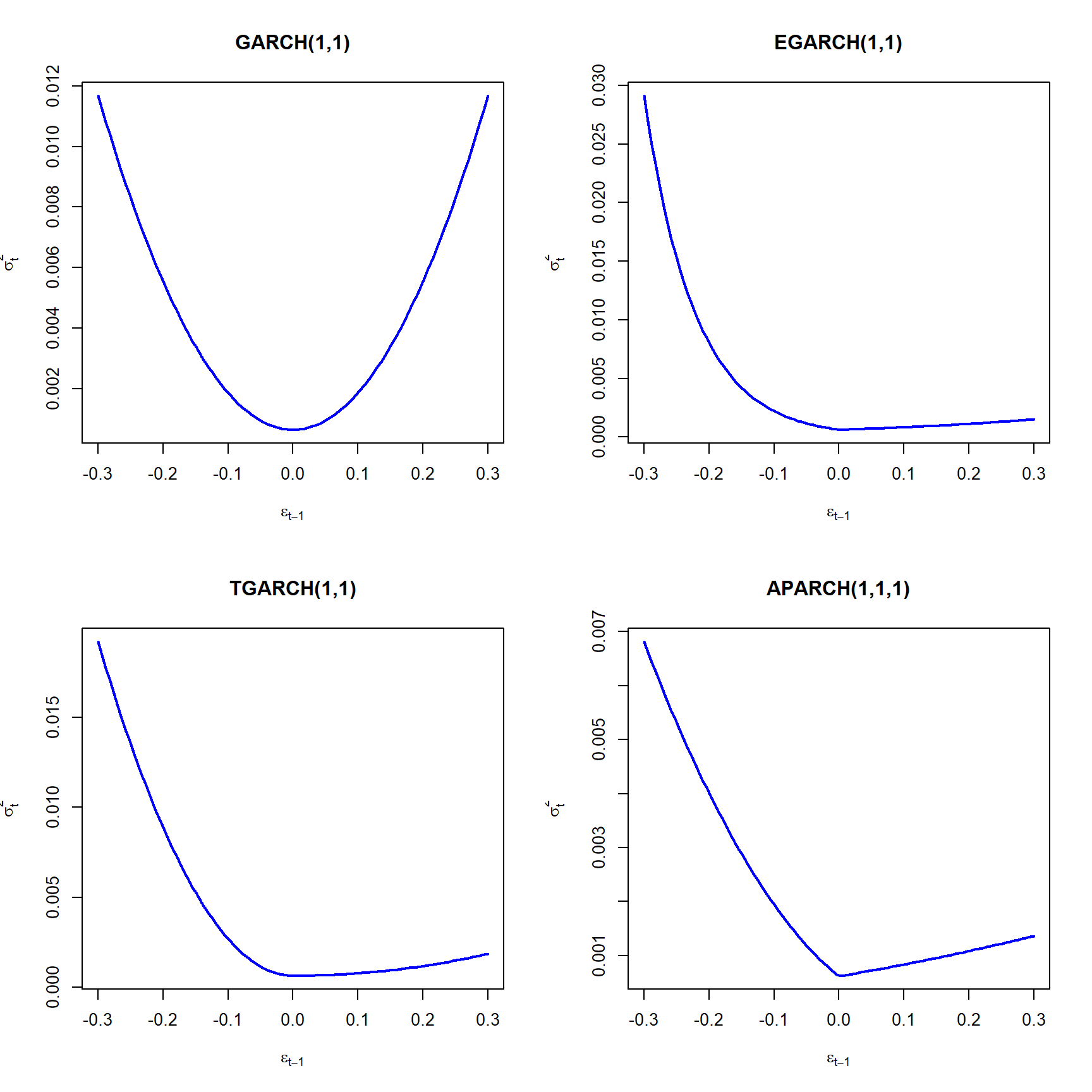

Comparando as News Impact Curves

nic.garch11 = newsimpact(VALE.garch11.fit)

nic.egarch11 = newsimpact(VALE.egarch11.fit)

nic.gjrgarch11 = newsimpact(VALE.gjrgarch11.fit)

nic.aparch11.1 = newsimpact(VALE.aparch11.1.fit)Via critério de informação, comparamos:

model.list = list(garch11 = VALE.garch11.fit,

egarch11 = VALE.egarch11.fit,

gjrgarch11 = VALE.gjrgarch11.fit,

aparch11.1 = VALE.aparch11.1.fit)

info.mat = sapply(model.list, infocriteria)

rownames(info.mat) = rownames(infocriteria(VALE.garch11.fit))

info.mat garch11 egarch11 gjrgarch11 aparch11.1

Akaike -4.446 -4.457 -4.462 -4.457

Bayes -4.431 -4.438 -4.443 -4.438

Shibata -4.446 -4.457 -4.462 -4.457

Hannan-Quinn -4.440 -4.450 -4.455 -4.450Mostra a News Impact Curve estimada GARCH(1,1) e EGARCH(1,1)

par(mfrow=c(2,2))

plot(nic.garch11$zx, type="l", lwd=2, col="blue", main="GARCH(1,1)",

nic.garch11$zy, ylab=nic.garch11$yexpr, xlab=nic.garch11$xexpr)

plot(nic.egarch11$zx, type="l", lwd=2, col="blue", main="EGARCH(1,1)",

nic.egarch11$zy, ylab=nic.egarch11$yexpr, xlab=nic.egarch11$xexpr)

plot(nic.gjrgarch11$zx, type="l", lwd=2, col="blue", main="TGARCH(1,1)",

nic.gjrgarch11$zy, ylab=nic.gjrgarch11$yexpr, xlab=nic.gjrgarch11$xexpr)

plot(nic.aparch11.1$zx, type="l", lwd=2, col="blue", main="APARCH(1,1,1)",

nic.aparch11.1$zy, ylab=nic.aparch11.1$yexpr, xlab=nic.aparch11.1$xexpr)

Modelo GARCH com erros não-normais

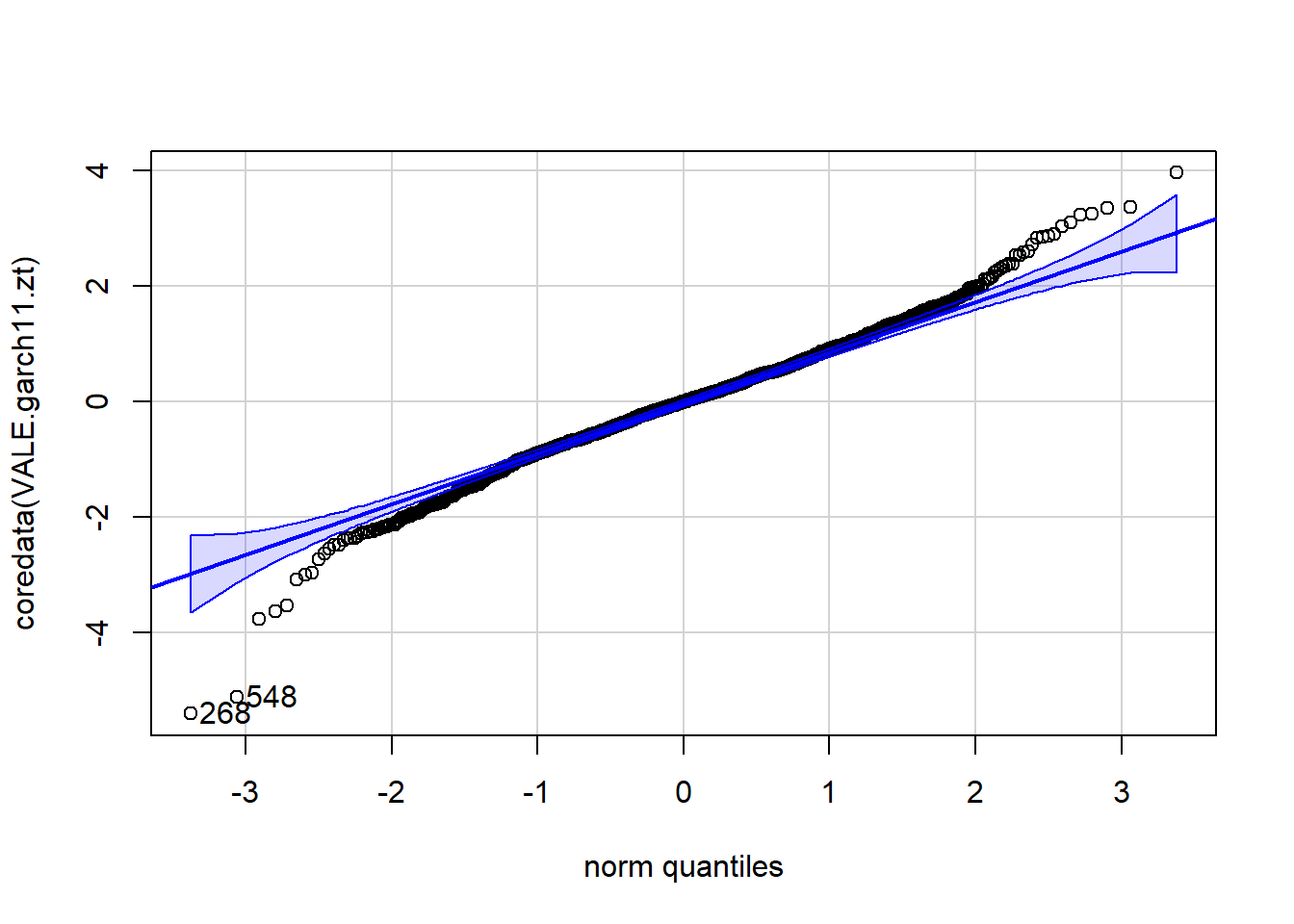

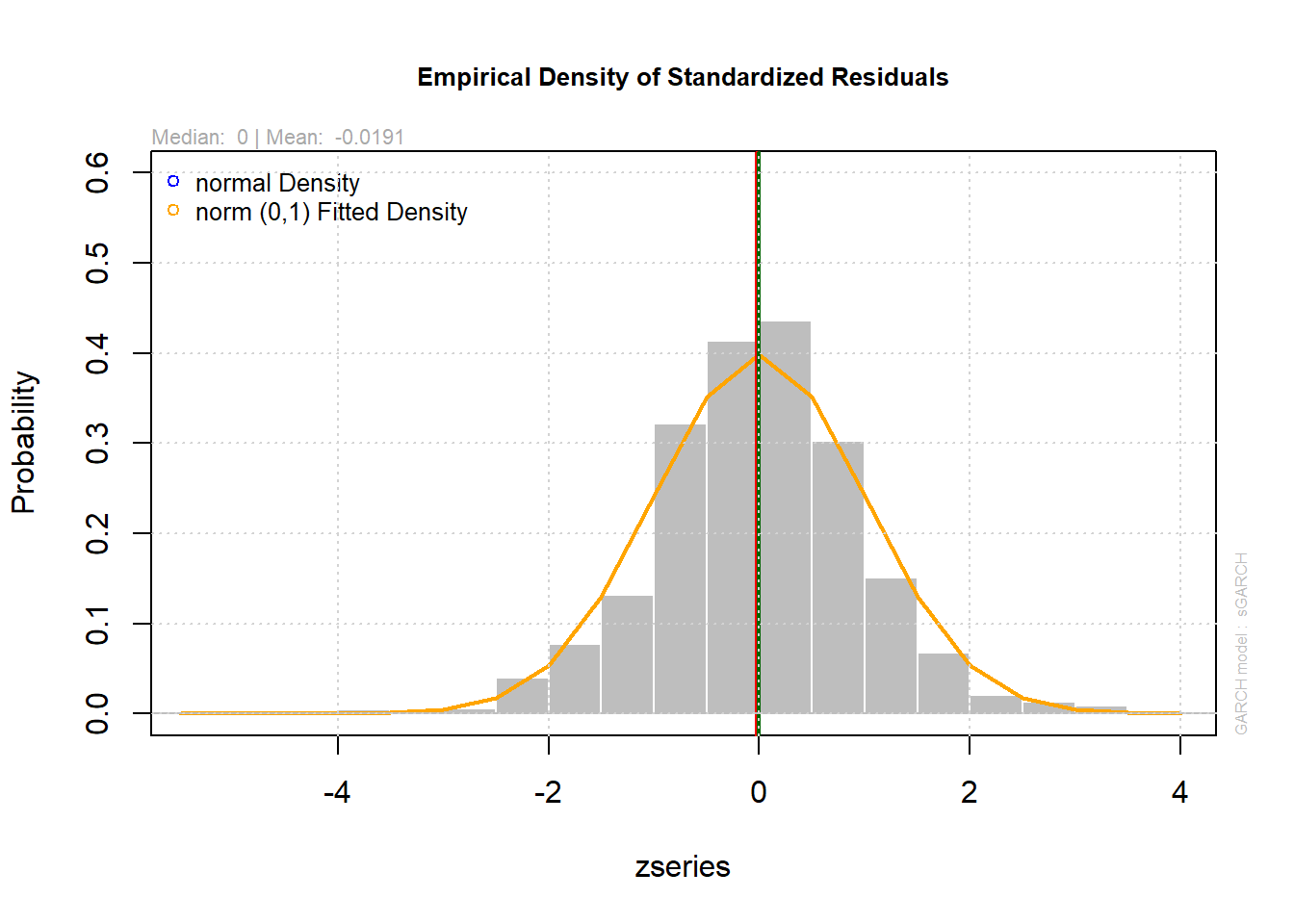

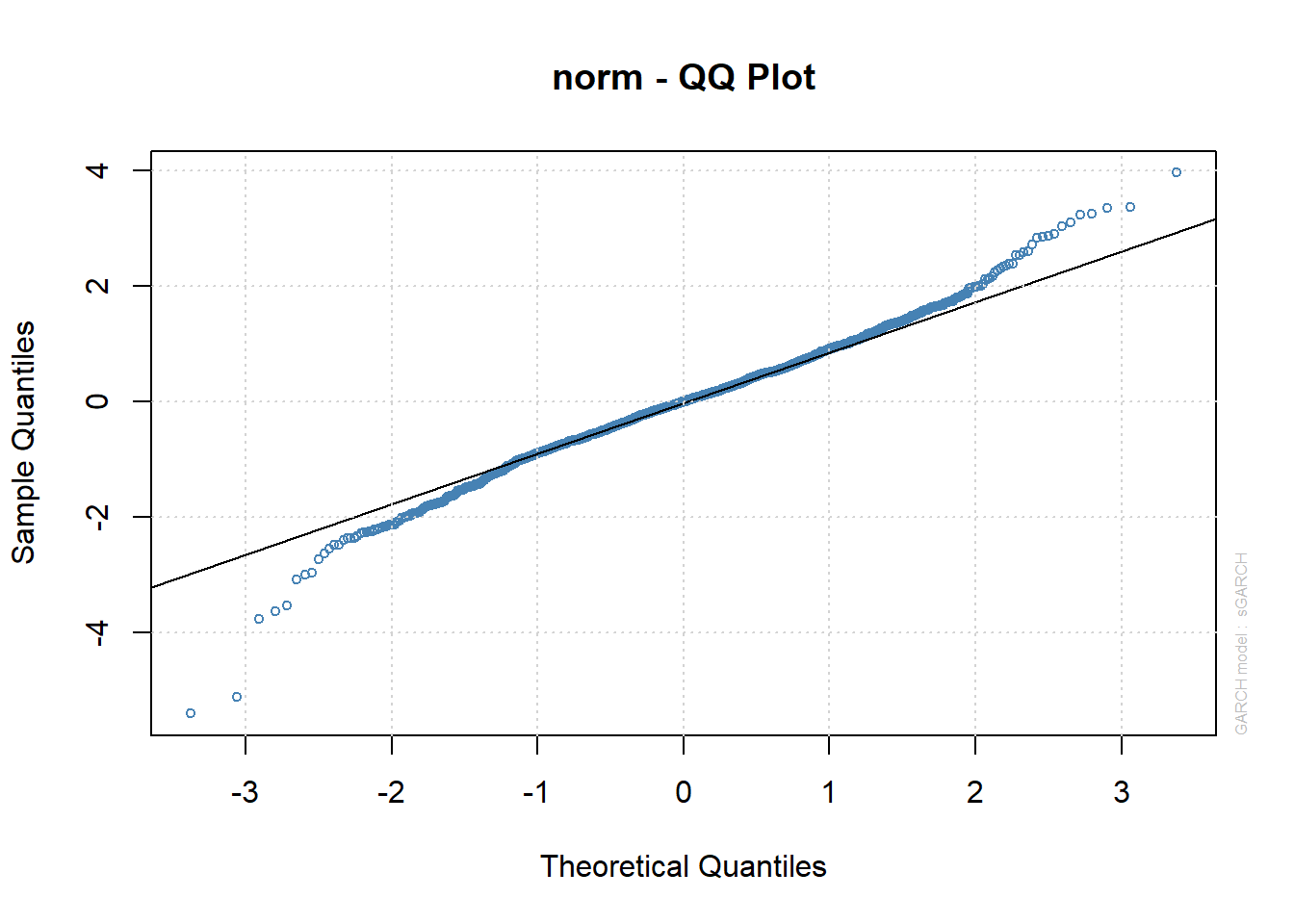

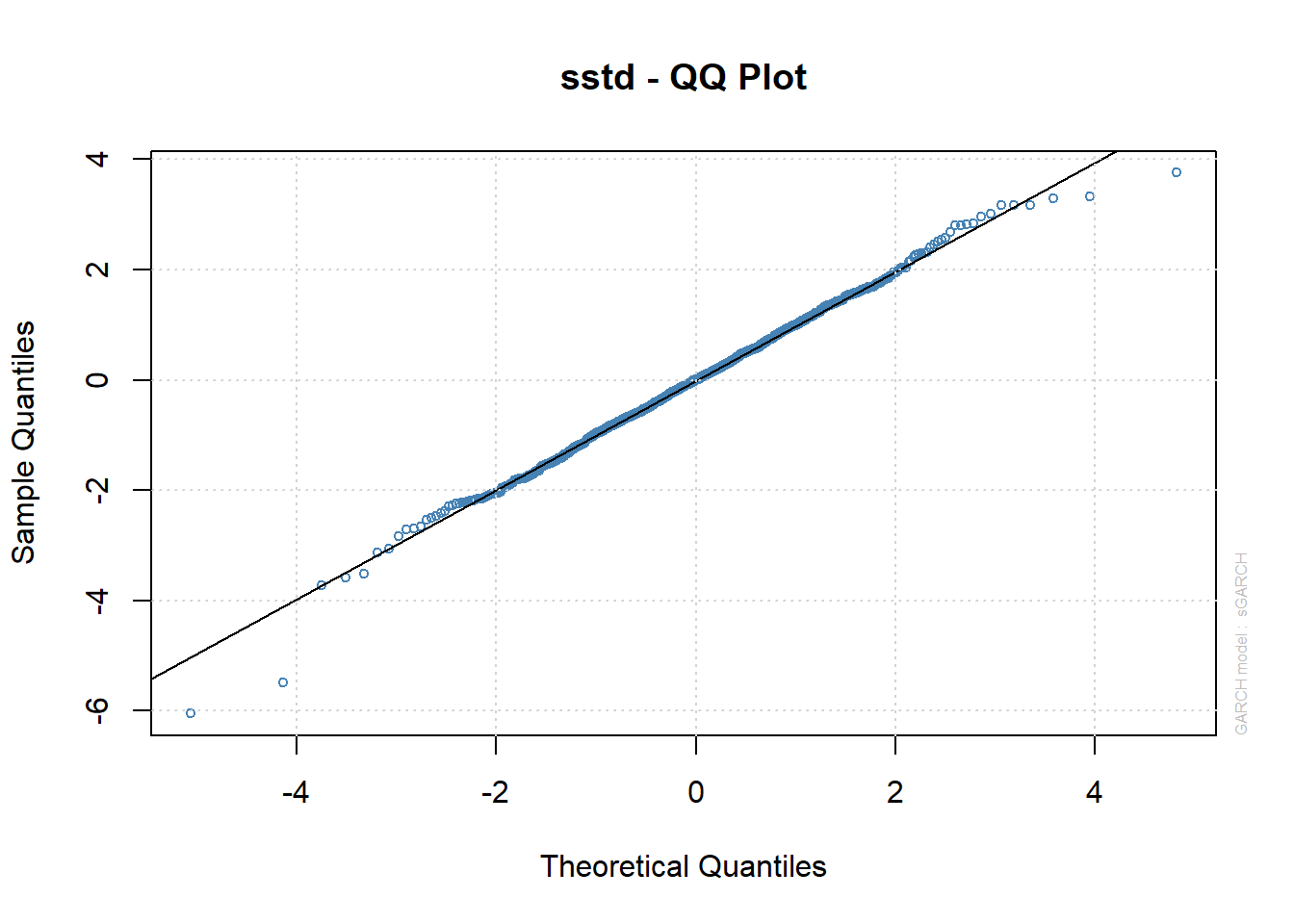

Vamos observar um modelo GARCH(1,1) normal, examinaremos os resíduos padronizados:

VALE.garch11.zt = residuals(VALE.garch11.fit)/sigma(VALE.garch11.fit)

VALE.garch11.zt = xts(VALE.garch11.zt, order.by=index(VALE.ret))

qqPlot(coredata(VALE.garch11.zt))

[1] 268 548plot(VALE.garch11.fit, which=8)

plot(VALE.garch11.fit, which=9)

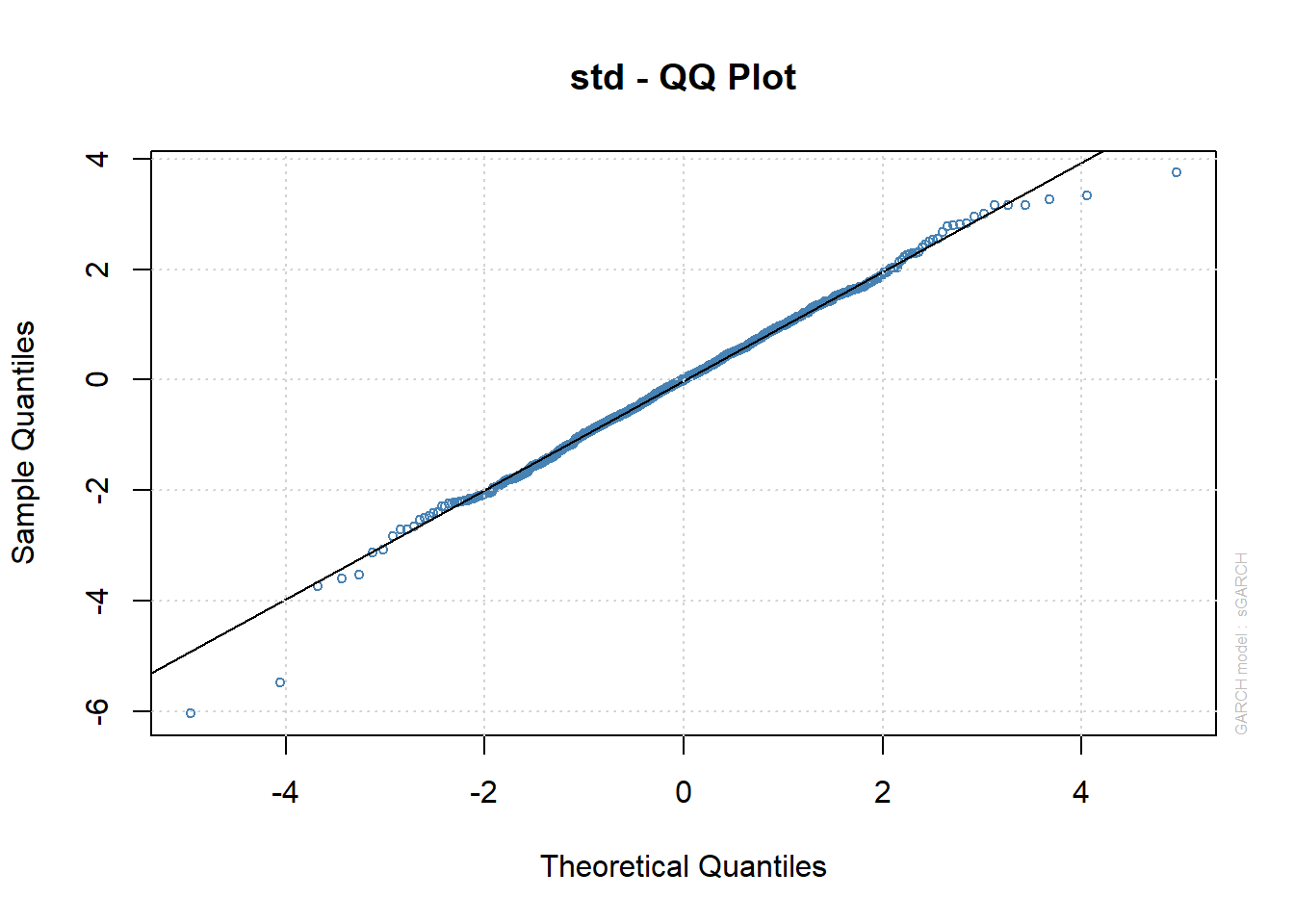

Rodaremos um modelo GARCH(1,1) com erros de Student \(t\):

garch11.t.spec = ugarchspec(variance.model = list(garchOrder=c(1,1)),

mean.model = list(armaOrder=c(0,0)),

distribution.model = "std")

VALE.garch11.t.fit = ugarchfit(spec=garch11.t.spec, data=VALE.ret)

VALE.garch11.t.fit

*---------------------------------*

* GARCH Model Fit *

*---------------------------------*

Conditional Variance Dynamics

-----------------------------------

GARCH Model : sGARCH(1,1)

Mean Model : ARFIMA(0,0,0)

Distribution : std

Optimal Parameters

------------------------------------

Estimate Std. Error t value Pr(>|t|)

mu 0.000510 0.000646 0.78967 0.429722

omega 0.000082 0.000032 2.52697 0.011505

alpha1 0.077329 0.023052 3.35461 0.000795

beta1 0.807590 0.060547 13.33824 0.000000

shape 6.563801 1.125766 5.83052 0.000000

Robust Standard Errors:

Estimate Std. Error t value Pr(>|t|)

mu 0.000510 0.000633 0.8060 0.420244

omega 0.000082 0.000035 2.3304 0.019786

alpha1 0.077329 0.037766 2.0476 0.040604

beta1 0.807590 0.072977 11.0664 0.000000

shape 6.563801 1.222901 5.3674 0.000000

LogLikelihood : 3075

Information Criteria

------------------------------------

Akaike -4.4887

Bayes -4.4696

Shibata -4.4887

Hannan-Quinn -4.4815

Weighted Ljung-Box Test on Standardized Residuals

------------------------------------

statistic p-value

Lag[1] 0.003734 0.9513

Lag[2*(p+q)+(p+q)-1][2] 0.281145 0.8063

Lag[4*(p+q)+(p+q)-1][5] 1.695005 0.6920

d.o.f=0

H0 : No serial correlation

Weighted Ljung-Box Test on Standardized Squared Residuals

------------------------------------

statistic p-value

Lag[1] 15.55 8.029e-05

Lag[2*(p+q)+(p+q)-1][5] 15.95 2.460e-04

Lag[4*(p+q)+(p+q)-1][9] 17.14 1.066e-03

d.o.f=2

Weighted ARCH LM Tests

------------------------------------

Statistic Shape Scale P-Value

ARCH Lag[3] 0.3973 0.500 2.000 0.5285

ARCH Lag[5] 0.6670 1.440 1.667 0.8335

ARCH Lag[7] 1.2800 2.315 1.543 0.8642

Nyblom stability test

------------------------------------

Joint Statistic: 0.8766

Individual Statistics:

mu 0.1006

omega 0.2864

alpha1 0.2121

beta1 0.3080

shape 0.3454

Asymptotic Critical Values (10% 5% 1%)

Joint Statistic: 1.28 1.47 1.88

Individual Statistic: 0.35 0.47 0.75

Sign Bias Test

------------------------------------

t-value prob sig

Sign Bias 1.453 1.465e-01

Negative Sign Bias 4.634 3.922e-06 ***

Positive Sign Bias 0.199 8.423e-01

Joint Effect 23.560 3.086e-05 ***

Adjusted Pearson Goodness-of-Fit Test:

------------------------------------

group statistic p-value(g-1)

1 20 19.98 0.3956

2 30 25.29 0.6631

3 40 28.14 0.9014

4 50 39.02 0.8456

Elapsed time : 0.3038 plot(VALE.garch11.t.fit, which=9)

aparch11.1.t.spec = ugarchspec(variance.model = list(model="apARCH",

garchOrder=c(1,1)),

mean.model = list(armaOrder=c(0,0)),

distribution.model = "std",

fixed.pars=list(delta=1))

VALE.aparch11.1.t.fit = ugarchfit(spec=aparch11.1.t.spec, data=VALE.ret)

VALE.aparch11.1.t.fit

*---------------------------------*

* GARCH Model Fit *

*---------------------------------*

Conditional Variance Dynamics

-----------------------------------

GARCH Model : apARCH(1,1)

Mean Model : ARFIMA(0,0,0)

Distribution : std

Optimal Parameters

------------------------------------

Estimate Std. Error t value Pr(>|t|)

mu 0.000145 0.000647 0.22422 0.822584

omega 0.002495 0.000967 2.57914 0.009905

alpha1 0.082988 0.021633 3.83616 0.000125

beta1 0.842620 0.047924 17.58228 0.000000

gamma1 0.603759 0.192088 3.14313 0.001671

delta 1.000000 NA NA NA

shape 6.795048 1.197332 5.67516 0.000000

Robust Standard Errors:

Estimate Std. Error t value Pr(>|t|)

mu 0.000145 0.000655 0.22145 0.824740

omega 0.002495 0.001224 2.03781 0.041569

alpha1 0.082988 0.025608 3.24064 0.001193

beta1 0.842620 0.060979 13.81829 0.000000

gamma1 0.603759 0.180442 3.34600 0.000820

delta 1.000000 NA NA NA

shape 6.795048 1.198521 5.66953 0.000000

LogLikelihood : 3081

Information Criteria

------------------------------------

Akaike -4.4961

Bayes -4.4732

Shibata -4.4961

Hannan-Quinn -4.4875

Weighted Ljung-Box Test on Standardized Residuals

------------------------------------

statistic p-value

Lag[1] 0.003469 0.9530

Lag[2*(p+q)+(p+q)-1][2] 0.340440 0.7736

Lag[4*(p+q)+(p+q)-1][5] 1.592027 0.7173

d.o.f=0

H0 : No serial correlation

Weighted Ljung-Box Test on Standardized Squared Residuals

------------------------------------

statistic p-value

Lag[1] 18.62 1.591e-05

Lag[2*(p+q)+(p+q)-1][5] 19.00 3.644e-05

Lag[4*(p+q)+(p+q)-1][9] 20.07 1.924e-04

d.o.f=2

Weighted ARCH LM Tests

------------------------------------

Statistic Shape Scale P-Value

ARCH Lag[3] 0.1486 0.500 2.000 0.6999

ARCH Lag[5] 0.3035 1.440 1.667 0.9393

ARCH Lag[7] 0.9906 2.315 1.543 0.9151

Nyblom stability test

------------------------------------

Joint Statistic: 0.8841

Individual Statistics:

mu 0.07869

omega 0.16672

alpha1 0.17589

beta1 0.16925

gamma1 0.11133

shape 0.30942

Asymptotic Critical Values (10% 5% 1%)

Joint Statistic: 1.49 1.68 2.12

Individual Statistic: 0.35 0.47 0.75

Sign Bias Test

------------------------------------

t-value prob sig

Sign Bias 1.7339 8.317e-02 *

Negative Sign Bias 4.1472 3.574e-05 ***

Positive Sign Bias 0.1362 8.917e-01

Joint Effect 17.3662 5.942e-04 ***

Adjusted Pearson Goodness-of-Fit Test:

------------------------------------

group statistic p-value(g-1)

1 20 15.95 0.6608

2 30 29.41 0.4438

3 40 24.05 0.9711

4 50 38.14 0.8690

Elapsed time : 1.231 plot(residuals(VALE.aparch11.1.t.fit))

Ajustamos uma \(t\) enviesada:

garch11.st.spec = ugarchspec(variance.model = list(garchOrder=c(1,1)),

mean.model = list(armaOrder=c(0,0)),

distribution.model = "sstd")

VALE.garch11.st.fit = ugarchfit(spec=garch11.st.spec, data=VALE.ret)

VALE.garch11.st.fit

*---------------------------------*

* GARCH Model Fit *

*---------------------------------*

Conditional Variance Dynamics

-----------------------------------

GARCH Model : sGARCH(1,1)

Mean Model : ARFIMA(0,0,0)

Distribution : sstd

Optimal Parameters

------------------------------------

Estimate Std. Error t value Pr(>|t|)

mu 0.000340 0.000683 0.49827 0.618294

omega 0.000080 0.000032 2.51984 0.011741

alpha1 0.076986 0.022903 3.36144 0.000775

beta1 0.809743 0.059818 13.53670 0.000000

skew 0.971957 0.036344 26.74360 0.000000

shape 6.592137 1.135063 5.80773 0.000000

Robust Standard Errors:

Estimate Std. Error t value Pr(>|t|)

mu 0.000340 0.000673 0.5054 0.613279

omega 0.000080 0.000034 2.3344 0.019573

alpha1 0.076986 0.037494 2.0533 0.040042

beta1 0.809743 0.072072 11.2351 0.000000

skew 0.971957 0.037452 25.9523 0.000000

shape 6.592137 1.221276 5.3977 0.000000

LogLikelihood : 3076

Information Criteria

------------------------------------

Akaike -4.4876

Bayes -4.4647

Shibata -4.4877

Hannan-Quinn -4.4790

Weighted Ljung-Box Test on Standardized Residuals

------------------------------------

statistic p-value

Lag[1] 0.003709 0.9514

Lag[2*(p+q)+(p+q)-1][2] 0.279837 0.8070

Lag[4*(p+q)+(p+q)-1][5] 1.692357 0.6926

d.o.f=0

H0 : No serial correlation

Weighted Ljung-Box Test on Standardized Squared Residuals

------------------------------------

statistic p-value

Lag[1] 15.44 8.529e-05

Lag[2*(p+q)+(p+q)-1][5] 15.84 2.634e-04

Lag[4*(p+q)+(p+q)-1][9] 17.04 1.132e-03

d.o.f=2

Weighted ARCH LM Tests

------------------------------------

Statistic Shape Scale P-Value

ARCH Lag[3] 0.3944 0.500 2.000 0.530

ARCH Lag[5] 0.6753 1.440 1.667 0.831

ARCH Lag[7] 1.2759 2.315 1.543 0.865

Nyblom stability test

------------------------------------

Joint Statistic: 1.289

Individual Statistics:

mu 0.0969

omega 0.2857

alpha1 0.2098

beta1 0.3087

skew 0.5322

shape 0.3299

Asymptotic Critical Values (10% 5% 1%)

Joint Statistic: 1.49 1.68 2.12

Individual Statistic: 0.35 0.47 0.75

Sign Bias Test

------------------------------------

t-value prob sig

Sign Bias 1.4998 1.339e-01

Negative Sign Bias 4.6772 3.197e-06 ***

Positive Sign Bias 0.2336 8.153e-01

Joint Effect 23.9089 2.610e-05 ***

Adjusted Pearson Goodness-of-Fit Test:

------------------------------------

group statistic p-value(g-1)

1 20 15.95 0.6608

2 30 25.42 0.6562

3 40 28.32 0.8970

4 50 36.02 0.9162

Elapsed time : 0.4376 plot(VALE.garch11.st.fit, which=9)

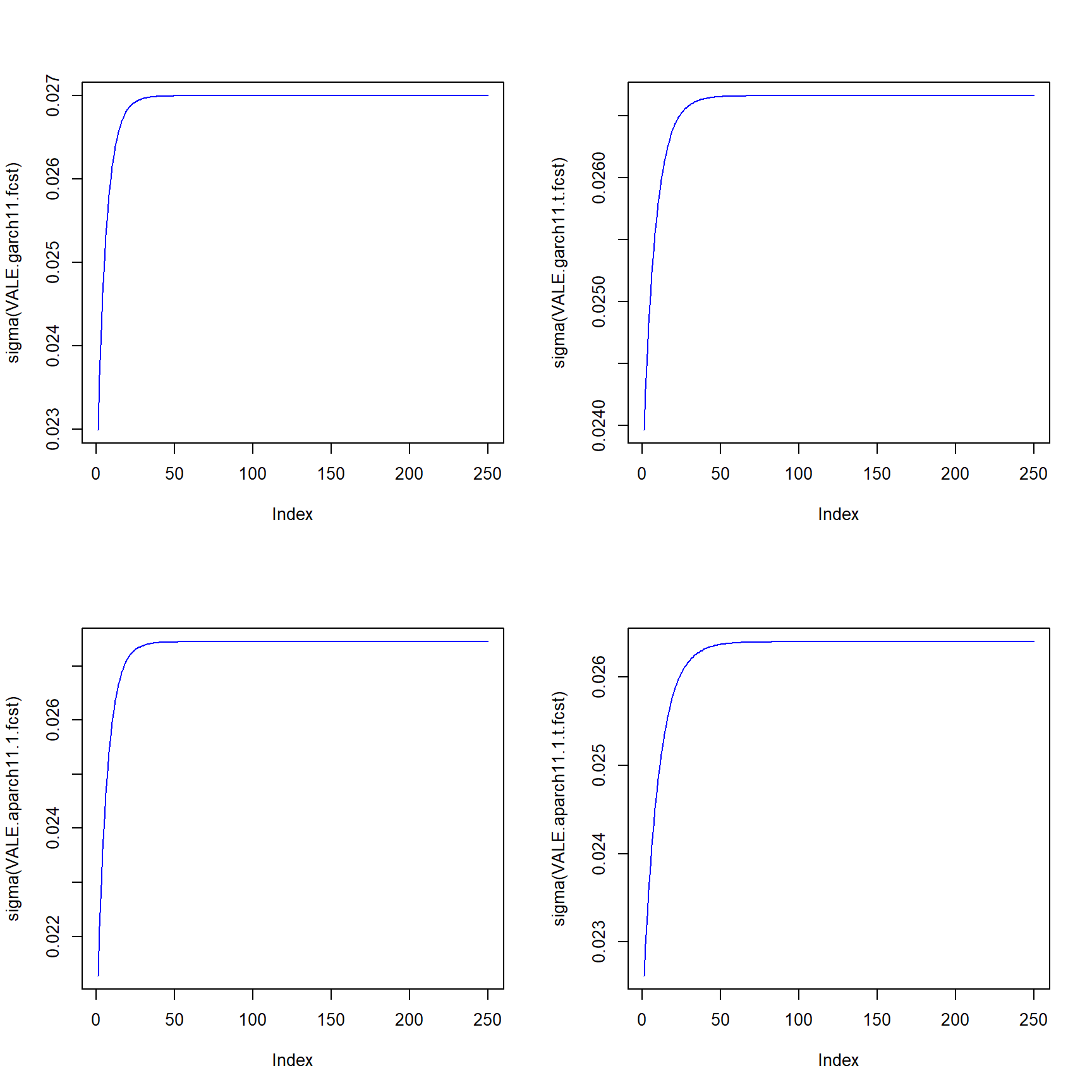

Plotamos os gráficos dos modelos da família ARCH

VALE.garch11.fcst = ugarchforecast(VALE.garch11.fit, n.ahead=250)

VALE.garch11.t.fcst = ugarchforecast(VALE.garch11.t.fit, n.ahead=250)

VALE.aparch11.1.fcst = ugarchforecast(VALE.aparch11.1.fit, n.ahead=250)

VALE.aparch11.1.t.fcst = ugarchforecast(VALE.aparch11.1.t.fit, n.ahead=250)Ploto os gráficos

par(mfrow=c(2,2))

plot(sigma(VALE.garch11.fcst), type="l", col="blue")

plot(sigma(VALE.garch11.t.fcst), type="l", col="blue")

plot(sigma(VALE.aparch11.1.fcst), type="l", col="blue")

plot(sigma(VALE.aparch11.1.t.fcst), type="l", col="blue")

Extraio as projeções de volatilidades:

#VALE.garch11.sigma = as.data.frame(VALE.garch11.fcst)$sigma

#VALE.garch11.t.sigma = as.data.frame(VALE.garch11.t.fcst)$sigma

#VALE.aparch11.1.sigma = as.data.frame(VALE.aparch11.1.fcst)$sigma

#VALE.aparch11.1.t.sigma = as.data.frame(VALE.aparch11.1.t.fcst)$sigma

#ymax = max(VALE.garch11.sigma,VALE.garch11.t.sigma,VALE.aparch11.1.sigma, VALE.aparch11.1.t.sigma)

#ymin = min(VALE.garch11.sigma,VALE.garch11.t.sigma,VALE.aparch11.1.sigma, VALE.aparch11.1.t.sigma)

#plot.ts(VALE.garch11.sigma, main="Projeções de Volatilidades",

# ylim=c(ymin,ymax), col="black",

# lwd=2, ylab="sigma(t+h|t)", xlab="h")

#lines(VALE.garch11.t.sigma, col="blue", lwd=2)

#lines(VALE.aparch11.1.sigma, col="green", lwd=2)

#lines(VALE.aparch11.1.t.sigma, col="red", lwd=2)

#legend(x="topleft", legend=c("GARCH-n", "GARCH-t", "APARCH-n", "APARCH-t"),

# col=c("black", "blue","green","red"), lwd=2, lty = "solid")Reajusta os modelos, deixando 100 observações fora da amostra para estatísticas de avaliação de previsão

VALE.garch11.fit = ugarchfit(spec=garch11.spec, data=VALE.ret,

out.sample=100)

VALE.garch11.t.fit = ugarchfit(spec=garch11.t.spec, data=VALE.ret,

out.sample=100)

VALE.aparch11.1.fit = ugarchfit(aparch11.1.spec, VALE.ret,

out.sample=100)

VALE.aparch11.1.t.fit = ugarchfit(spec=aparch11.1.t.spec, data=VALE.ret,

out.sample=100)Compara a persistência com a variância incondicional:

c.mat = matrix(0, 4, 2)

colnames(c.mat) = c("Persistence", "E[sig(t)]")

rownames(c.mat) = c("GARCH-n", "GARCH-t", "APARCH-n","APARCH-t")

c.mat["GARCH-n","Persistence"] = persistence(VALE.garch11.fit)

c.mat["GARCH-t","Persistence"] = persistence(VALE.garch11.t.fit)

c.mat["APARCH-n","Persistence"] = persistence(VALE.aparch11.1.fit)

c.mat["APARCH-t","Persistence"] = persistence(VALE.aparch11.1.t.fit)

c.mat["GARCH-n","E[sig(t)]"] = sqrt(uncvariance(VALE.garch11.fit))

c.mat["GARCH-t","E[sig(t)]"] = sqrt(uncvariance(VALE.garch11.t.fit))

c.mat["APARCH-n","E[sig(t)]"] = sqrt(uncvariance(VALE.aparch11.1.fit))

c.mat["APARCH-t","E[sig(t)]"] = sqrt(uncvariance(VALE.aparch11.1.t.fit))

c.mat Persistence E[sig(t)]

GARCH-n 0.8402 0.02746

GARCH-t 0.8746 0.02709

APARCH-n 0.8522 0.02784

APARCH-t 0.8992 0.02672Finaliza computando 100 previsões dinâmicas 1 passo à frente:

VALE.garch11.fcst = ugarchforecast(VALE.garch11.fit, n.roll=100, n.ahead=1)

VALE.garch11.t.fcst = ugarchforecast(VALE.garch11.t.fit, n.roll=100, n.ahead=1)

VALE.aparch11.1.fcst = ugarchforecast(VALE.aparch11.1.fit, n.roll=100, n.ahead=1)

VALE.aparch11.1.t.fcst = ugarchforecast(VALE.aparch11.1.t.fit, n.roll=100, n.ahead=1)Vamos ver os resultados para os retornos esperados pelos 4 modelos ajustados:

VALE.garch11.fcst

*------------------------------------*

* GARCH Model Forecast *

*------------------------------------*

Model: sGARCH

Horizon: 1

Roll Steps: 100

Out of Sample: 1

0-roll forecast [T0=2023-01-17]:

Series Sigma

T+1 0.0008252 0.02441VALE.garch11.t.fcst

*------------------------------------*

* GARCH Model Forecast *

*------------------------------------*

Model: sGARCH

Horizon: 1

Roll Steps: 100

Out of Sample: 1

0-roll forecast [T0=2023-01-17]:

Series Sigma

T+1 0.0008341 0.02453VALE.aparch11.1.fcst

*------------------------------------*

* GARCH Model Forecast *

*------------------------------------*

Model: apARCH

Horizon: 1

Roll Steps: 100

Out of Sample: 1

0-roll forecast [T0=2023-01-17]:

Series Sigma

T+1 2.16e-05 0.02453VALE.aparch11.1.t.fcst

*------------------------------------*

* GARCH Model Forecast *

*------------------------------------*

Model: apARCH

Horizon: 1

Roll Steps: 100

Out of Sample: 1

0-roll forecast [T0=2023-01-17]:

Series Sigma

T+1 0.0004423 0.02365Com os dados observados, comparamos o de melhor ajuste:

# Obtem comparativo de previsao estatistica

fcst.list = list(garch11=VALE.garch11.fcst,

garch11.t=VALE.garch11.t.fcst,

aparch11.1=VALE.aparch11.1.fcst,

aparch11.t.1=VALE.aparch11.1.t.fcst)

fpm.mat = sapply(fcst.list, fpm)

fpm.mat garch11 garch11.t aparch11.1 aparch11.t.1

MSE 0.0004522 0.0004523 0.0004476 0.0004498

MAE 0.01625 0.01625 0.01612 0.01618

DAC 0.43 0.43 0.43 0.43 Referências

Graves, Spencer. 2014. FinTS: Companion to Tsay (2005) Analysis of Financial Time Series. https://CRAN.R-project.org/package=FinTS.

Ghalanos, Alexios. 2015. Rugarch: Univariate Garch Models. https://CRAN.R-project.org/package=rugarch.